Are you a self-employed individual or a small business owner looking for a retirement savings plan that meets your unique needs? If so, a Simplified Employee Pension (SEP) IRA might be the perfect solution to maximize your retirement savings.

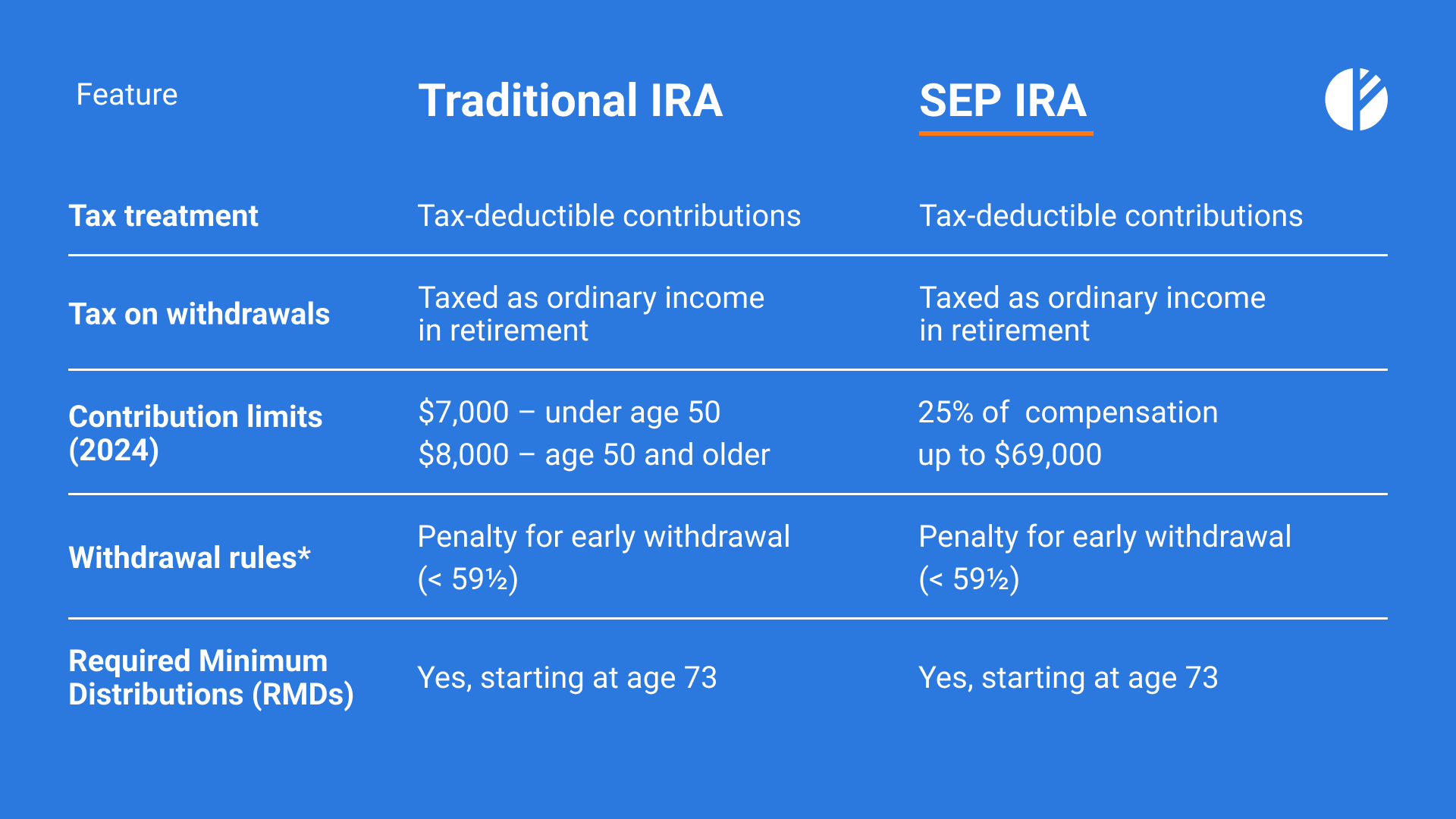

*Exceptions: first-time home purchase (up to $10,000 penalty-free), education expenses (up to $10,000 penalty-free), medical expenses, disability, death.

SEP IRAs allow contributions exclusively from the employer. Tax benefits apply to business earnings, which can reduce a company's taxable income.

Key benefits

- High contribution limits up to $69,000

- Favorable tax treatment: earnings on the investment grow tax-deferred until withdrawn

- Flexibility: employers can contribute a percentage of employees' compensation, and contributions can vary from year to year

- Simplicity and low administrative costs

10% of small businesses offering retirement plans use a SEP IRA, reflecting its popularity due to its simplicity and flexibility.

Better suited for

To open a SEP IRA, you must be

a self-employed individual or a small business owner. This includes sole proprietors, independent contractors, and partners in a partnership.

In 2022, most SEP IRA contributions were made by

small businesses1.

While you’re not required to contribute to your employees’ SEP IRAs, doing so can provide a valuable benefit and potentially attract and retain top talent.

While SEP IRAs offer significant benefits, they may not be the ideal choice for everyone. Individuals who prefer to contribute to gftheir own retirement savings rather than rely on employer contributions might find SEP IRAs less appealing.

Those with complex financial situations or specific retirement goals may benefit from exploring other retirement plan options.

While SEP IRAs may not be ideal for everyone, their simplicity and employer-driven contributions make them especially attractive to small businesses aiming to offer retirement benefits while managing administrative costs effectively.

Imperial Fund Asset Management is a SEC-registered investment adviser.

SEC registration does not imply a certain level of skill or training.

The information provided is for informational purposes only and should not be considered investment advice or a solicitation to buy or sell any securities.

All investments involve risk, including the possible loss of principal. Please review our

full disclaimer for additional information.