In April 2026, the U.S. economy displayed a mix of re-accelerating inflation pressures, resilient growth momentum, and a powerful rebound across financial markets.

Macroeconomic Review

Inflation

In March, CPI jumped to 3.3% year-over-year – up sharply from 2.4% in February – driven substantially by the soaring energy prices. Core CPI, which strips out energy, rose a far more modest 2.6%, only a touch above February's 2.5%.

The Fed's preferred gauge told much the same story. PCE hit 3.5% year-over-year in March, its highest level since August 2023, while core PCE climbed to 3.2% – the fastest pace since late 2023.

This inflation backdrop suggests the Fed is likely to remain on hold for the foreseeable future.

Rising energy prices, fueled by geopolitical tensions involving Iran, have been the primary driver of the pickup in inflation.

In March, energy-related categories accounted for a substantial portion of the overall increase in consumer prices – more than the combined contributions from healthcare, motor vehicles, financial services, and insurance.

GDP

The U.S. economy showed meaningful signs of recovery in the first quarter of 2026.

Real GDP grew at an annualized rate of 2.0%, a significant rebound from the sluggish 0.5% recorded in the fourth quarter of 2025, though falling slightly short of economists' expectations of around 2.2%.

The core drivers of the recovery are the continued buildout of AI infrastructure and the early effects of recent tax cuts beginning to filter through the broader economy.

Looking ahead, the Atlanta Fed's GDPNow model forecasts growth accelerating to 3.7% in the second quarter.

Federal Reserve Policy

At its April 28–29 meeting, the Federal Reserve held rates unchanged at 3.50%–3.75%, marking the third consecutive hold as policymakers navigate ongoing geopolitical and economic uncertainty.

The decision itself came as no surprise, but the dynamics beneath the surface told a more complicated story.

For the first time since October 1992, there were four dissents.

Governor Stephen Miran pushed for an outright rate cut, while Cleveland Fed President Beth Hammack, Minneapolis Fed President Neel Kashkari, and Dallas Fed President Lorie Logan resisted any dovish language that might signal future cuts.

According to the CME Fed Watch tool, markets now assign a 72% probability that the Fed will not make any rate move before year-end.

This reflects the challenging backdrop: the ongoing conflict in the Middle East continues to weigh on economic visibility, elevated energy prices are filtering through the economy, and inflation remains stubbornly sticky.

The meeting also marked what is almost certainly Jerome Powell’s final chapter as Chair. The Senate Banking Committee advanced Kevin Warsh’s nomination, with full Senate confirmation expected the week of May 11.

In a notable twist, Powell announced he will not be leaving the Fed entirely – he intends to remain on the Board of Governors until a DOJ investigation into Federal Reserve renovations is resolved, with his term running through January 2028.

Manufacturing

Manufacturing activity expanded for a fourth consecutive month in April, with the ISM Manufacturing PMI holding steady at 52.7%, unchanged from March and the strongest sustained stretch since mid-2022.

The overall economy continued in expansion for the 18th consecutive month.

Demand indicators remained broadly supportive. The New Orders Index edged up 0.6 points to 54.1%, marking its fourth straight month of expansion. The Backlog of Orders Index slipped 3 points to 51.4%, remaining in expansion.

New Export Orders fell further into contraction at 47.9%, down 2 points, as trade and conflict-related frictions continued to weigh on international business.

On the output side, the Production Index expanded for a sixth consecutive month at 53.4%, though it cooled 1.7 points from March's 55.1%.

The Employment Index deteriorated further to 46.4%, down 2.3 points, extending its contraction streak to 31 months.

The most significant development in April was a continued surge in input costs. The Prices Index jumped another 6.3 points to 84.6%, its highest reading since April 2022 and a staggering 25.6-point cumulative increase over just three months.

Supplier Deliveries slowed further to 60.6%, the fifth consecutive month of deteriorating lead times, while Inventories contracted modestly at 49.0% and Customers' Inventories remained firmly in "too low" territory at 39.1%.

Labor Market

Total nonfarm payroll employment increased by 178,000 in March, reversing the decline of 133,000 recorded in February.

Job gains were primarily concentrated in healthcare, construction, transportation and warehousing, while federal government employment continued to decline.

The March print came in well ahead of expectations, surpassing the Dow Jones consensus estimate of 59,000 by a wide margin and marking the strongest monthly gain since the end of 2024.

The unemployment rate in March edged lower to 4.3% down from 4.4% in February.

Cross-Asset Performance Review

Equity

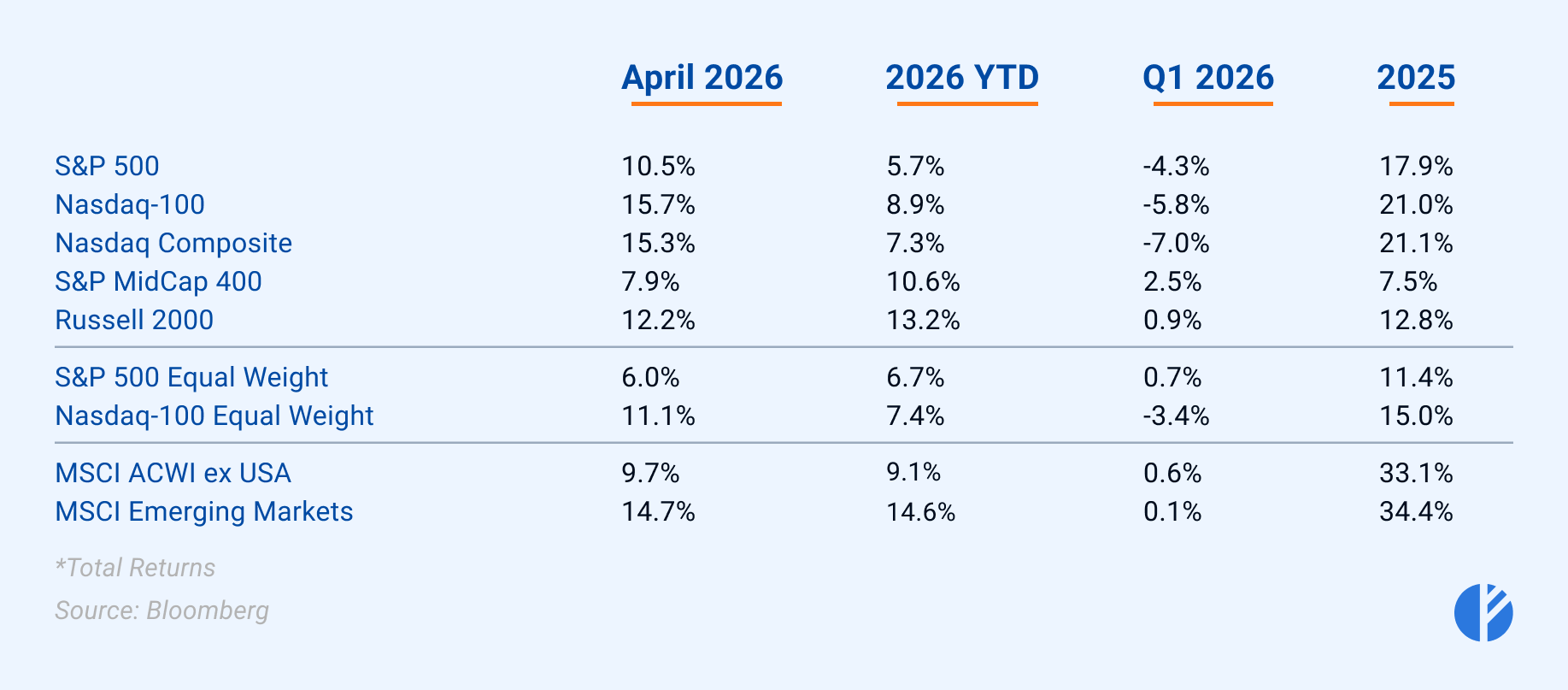

Equity markets staged a powerful rebound in April, emerging from March’s depressed and oversold levels to close the month at all-time highs across major U.S. indices.

The rally was underpinned by robust corporate earnings and renewed enthusiasm for artificial intelligence.

The Nasdaq-100 led the charge, surging 15.7% for its strongest monthly performance since 2002.

The S&P 500 climbed 10.5%, finishing April at a record 7,209 – marking its best monthly gain since November 2020 and pushing the index more than 20% higher over the past year.

Smaller stocks also joined the rally, with the Russell 2000 rising 12.2% and the S&P MidCap 400 advancing 7.9%, delivering broad participation across the market capitalization spectrum.

International equities also joined the rally with strong gains. Developed markets rose 9.7%, while emerging markets posted an even stronger 14.7% gain.

That said, performance remained heavily concentrated at the top, with capitalization-weighted indices meaningfully outperforming their equal-weighted counterparts.

This divergence once again highlighted the dominant influence of mega cap technology stocks.

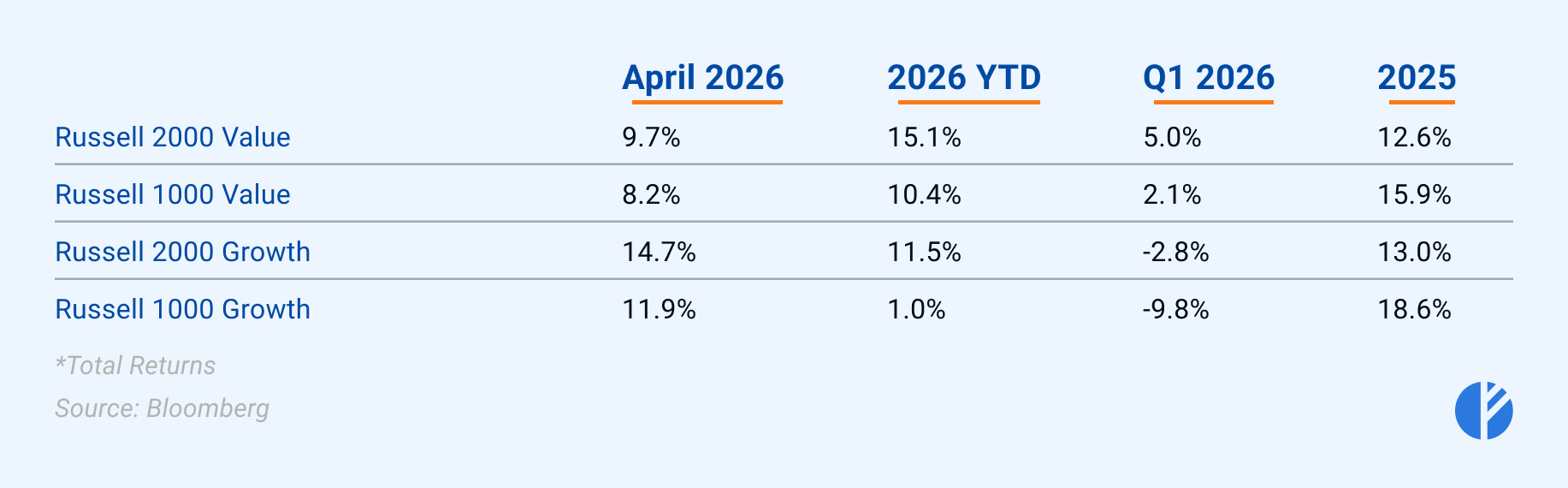

Both growth and value styles posted strong absolute returns in April, but growth clearly led the way.

Large- and small-cap growth indexes benefited from renewed investor confidence in secular themes such as artificial intelligence, cloud infrastructure, and semiconductors, where momentum and earnings visibility improved significantly during the month.

Value stocks also participated in the rally, supported by broad risk appetite and improving sentiment across cyclical sectors.

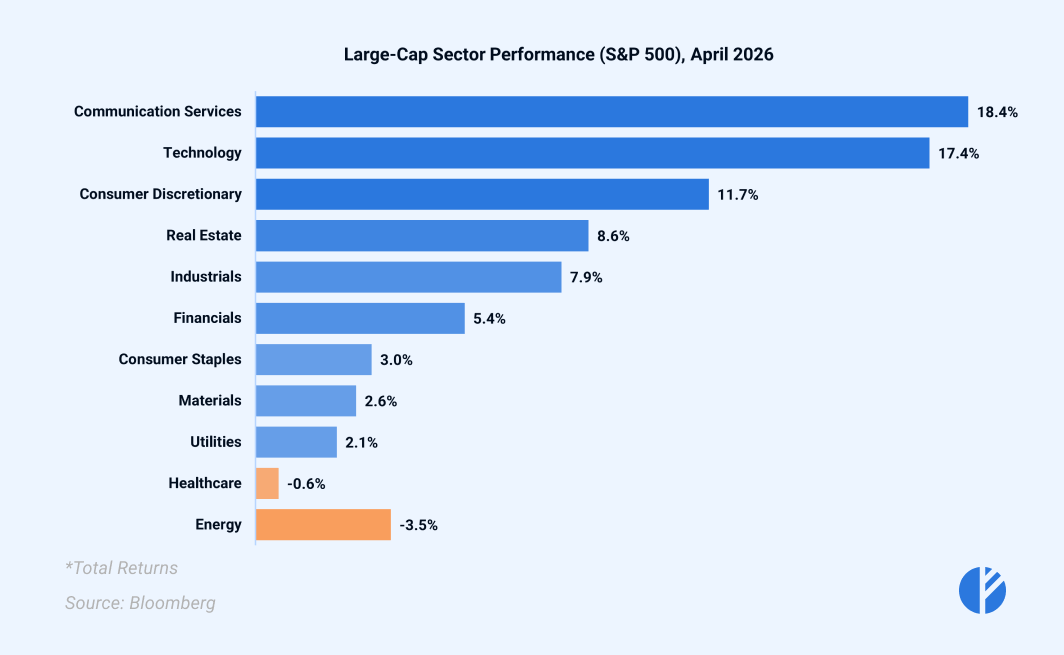

Large-cap sector performance in April reflected broad participation across most sectors and a clear reassertion of growth leadership.

Nine of the eleven S&P 500 sectors finished the month in positive territory, highlighting a healthy risk-on environment.

Communication Services and Technology led the market with strong returns of 18.4% and 17.4%, respectively.

The sectors benefited from improved investor sentiment toward semiconductors, artificial intelligence, and broader technology themes.

Cyclical sectors also participated meaningfully in the rebound.

Consumer Discretionary posted a robust 11.7%, while Real Estate advanced 8.6% and Industrials rose 7.9%.

Within Industrials, gains were concentrated in companies tied to automation, electrification, aerospace, and defense, supported by infrastructure spending, reshoring trends, and improving manufacturing activity.

Financials delivered a solid 5.4% gain, aided by stabilizing equity markets and renewed risk appetite that boosted trading and capital markets activity.

Defensive sectors, on the other hand, lagged during the risk-on reversal. Healthcare declined 0.6%, while Consumer Staples, Utilities, and Materials delivered modest gains of 2%–3%, reflecting reduced demand for traditional defensiveness.

Energy was the only clear laggard, falling 3.5% for the month. Despite a late-month rise in energy prices, the sector recovered after earlier overbought conditions.

Even with the April decline, Energy remains strongly up 33% year-to-date.

Fixed Income

Treasury yields rose modestly in April, as the oil shock reignited inflation concerns and shifted market expectations around the future path of interest rates.

The 1-year yield climbed 4 basis points to 3.68%, the 2-year rose 9 basis points, and the 10-year ended the month 10 basis points higher at 4.40%, its highest level since July 2025.

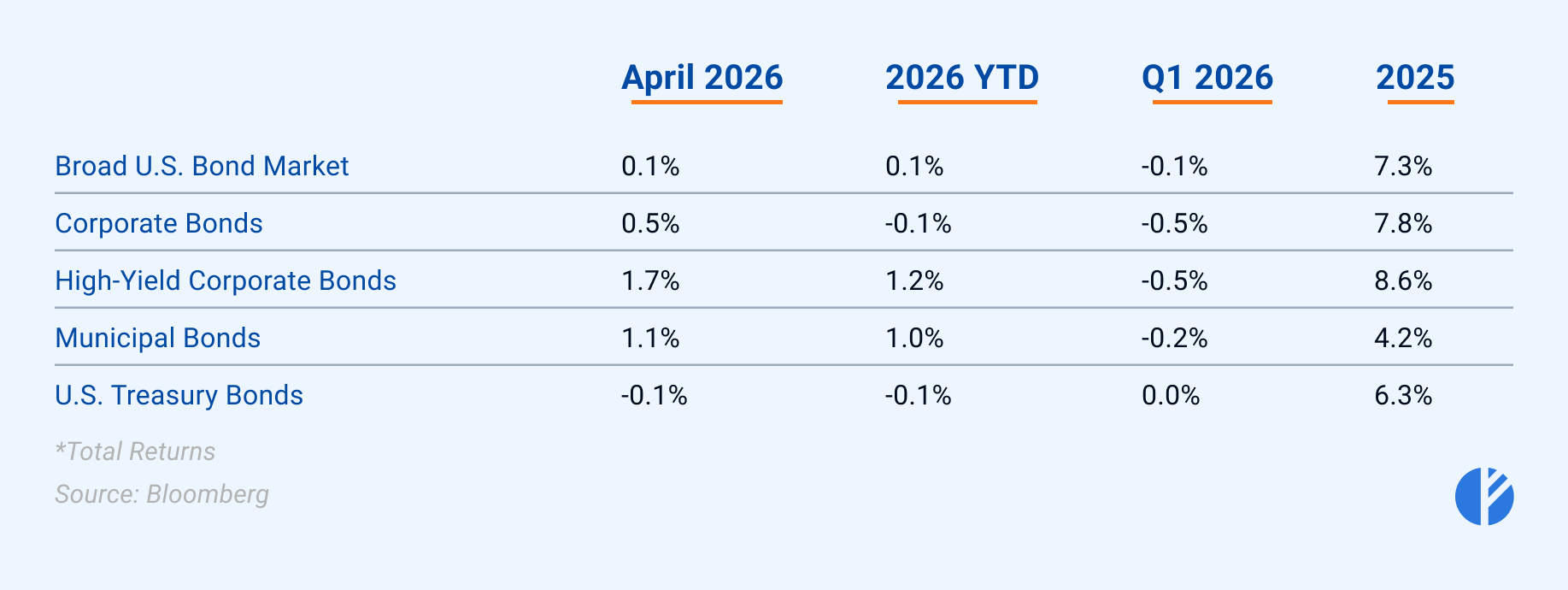

Despite the rise in yields, risk-on sentiment prevailed across credit markets.

High-Yield Corporate Bonds led with a gain of 1.7%, followed by Municipal Bonds at 1.1%, both rebounding from oversold conditions in March.

Investment-Grade Corporate Bonds added a modest 0.5%, while the Broad U.S. Bond Market eked out just 0.1%, weighed down by its heavy Treasury exposure. U.S.

Treasury Bonds were the sole laggard at 0.1%, as rising yields pressured prices and investors rotated toward higher-yielding alternatives.

Consistent with the broader risk appetite, investment-grade and high-yield corporate spreads compressed meaningfully during the month, narrowing by 9bps and 45bps to end at 81bps and 283bps, respectively.

FX and Oil Markets

Currency

The U.S. dollar ended April little changed and somewhat disappointing relative to expectations. The DXY Index fell from month-start highs near 100 to close around 98, effectively returning to pre-Iran conflict levels.

Despite the muted performance, several fundamental tailwinds should have supported the greenback: a solidly growing U.S. economy,

significantly lower exposure to the Middle East energy shock relative to Europe and Asia, and the Federal Reserve’s hawkish stance, which has delayed rate cuts and reinforced higher-for-longer interest rate expectations.

Crude Oil

Oil prices were sharply volatile throughout the month, with both major benchmarks swinging aggressively across wide ranges as geopolitical developments dictated market direction at every turn.

West Texas Intermediate (WTI) front-month futures traded between roughly $82 and $112 per barrel, while Brent crude swung in a $90 to $109 per barrel range.

The prolonged closure of the Strait of Hormuz dramatically reduced the availability of oil supplies to global markets, triggering cascading effects across supply chains that kept traders on edge throughout the period.

This article draws on data and insights from the U.S. Bureau of Labor Statistics (BLS), the United States Joint Economic Committee, the Institute for Supply Management (ISM), the Federal Reserve Bank of Atlanta,

Bloomberg, and FRED (Federal Reserve Economic Data), as well as leading financial publications including Barron’s, CNBC, CNN, MarketWatch, Nasdaq, Seeking Alpha, and The Economic Times.