In September, financial markets surged, driven by the Federal Reserve’s rate cut and heightened optimism around growth-driven sectors like Technology and Communication Services.

All major U.S. indexes reached new all-time highs, signaling strong investor confidence in the broader market.

Sectors such as Consumer Discretionary and Utilities performed solidly, cyclical sectors showed mixed results, with Materials and Consumer Staples trailing behind.

Treasury yields declined across the curve, underscoring expectations for continued monetary easing.

Major headlines

FOMC Meeting

The Federal Reserve announced on September 17 a 25-basis-point rate cut1, lowering the target range to 4.00%–4.25% from 4.25%–4.50% — its first reduction since December 2024.

According to the Summary of Economic Projections (SEP), policymakers anticipate two additional cuts in 2025 and one more in 2026, signaling a gradual easing path rather than an abrupt shift in policy.

During the press conference, Chair Jerome Powell noted that the decision reflects the Fed’s effort to address rising downside risks to employment and persistently elevated inflation.

Government Shutdown

On October 1, 2025, the U.S. government entered a shutdown2 after Congress failed to reach an agreement on a new funding bill.

The shutdown resulted from disagreements between Democrats and Republicans over issues such as healthcare subsidies and federal spending levels.

This shutdown, which marks the first of its kind since 2018, also had significant economic implications, with projections indicating a potential loss of $15 billion in GDP for every week it continues.

While essential services like Social Security and national defense remained operational, disruptions in other sectors, including research and public health, are widespread.

Macroeconomic Review

GDP

The third estimate shows 2Q GDP expanding at an annual rate of 3.8%3,

higher than the second estimate of 3.3% and the initial 3.0%. At the same time, first-quarter GDP was revised down slightly to an annual rate of -0.6% from -0.5%.

The rebound in the second quarter was primarily fueled by reduced imports and an increase in consumer spending.

Federal Reserve Policy

Federal Reserve cut its benchmark interest rate4 following the FOMC meeting on September 17-18, policymakers reduced the target range by 25 basis points to 4.00%–4.25%.

Inflation

Manufacturing

The ISM Manufacturing PMI inched up to 49.1% in September from 48.7% in August7, signaling continued contraction in manufacturing.

Meanwhile, the broader economy marked its 65th consecutive month of expansion since April 2020.

- New Orders fell back into contraction at 48.9% (down from 51.4%).

- Production strengthened to 51% (up from 47.8%).

- Prices remained elevated at 61.9% (down from 63.7%).

- Backlogs improved slightly to 46.2% (from 44.7%).

- Employment ticked higher to 45.3% (from 43.8%) but stayed weak.

Labor Market

Cross-Asset Performance Review

Equity Market Performance

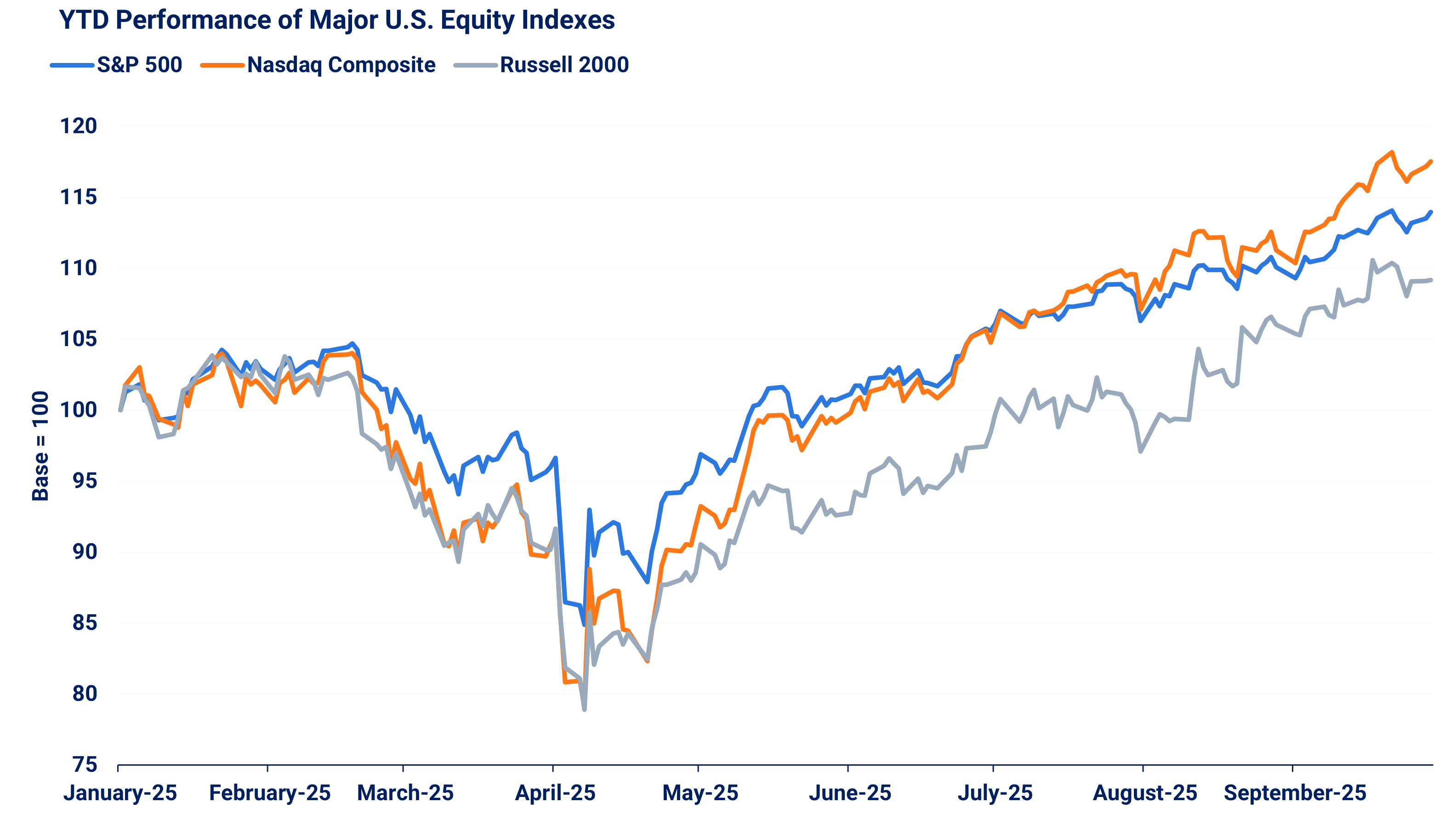

Markets rallied broadly in September, with all major U.S. indexes reaching new all-time highs.

The S&P 500 advanced 3.53%9,

the Russell 2000 gained 2.96%10,

and

the tech-heavy Nasdaq Composite surged 5.61%11.

Strength extended beyond the U.S. as well, with developed international markets performing solidly –

the MSCI World ex USA Index rose 2.17% over the month12.

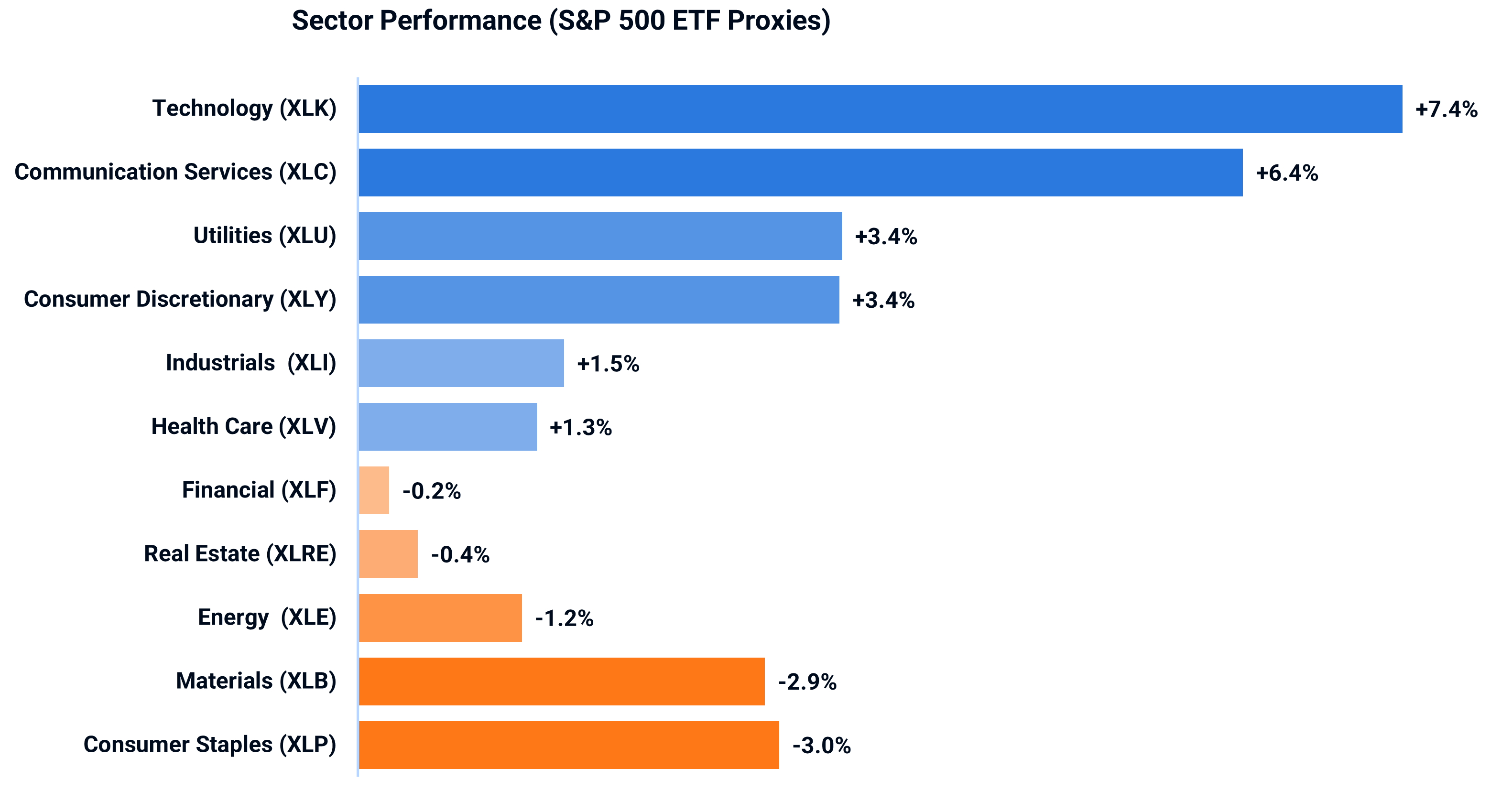

Sector Highlights

The current environment, created by the ongoing easing environment has strengthened investors’ appetite for growth-oriented assets.

Technology (

XLK13)

and Communication Services (

XLC14) led the market higher in September,

advancing roughly 7% and 6%, respectively, supported by

continued enthusiasm around artificial intelligence15

and

strong performance from industries’ leaders16.

Consumer Discretionary (

XLY17)

and Utilities (

XLU18) also posted solid gains of over 3%,

while Industrials (

XLI19)

and Health Care (

XLV20) each rose by more than 1%.

In contrast, Financials (

XLF21),

Real Estate (

XLRE22),

and Energy (

XLE23) edged lower, with declines of up to 1%.

The main laggards were Materials (

XLB24)

and Consumer Staples (

XLP25), both down about 3% for the month.

Fixed Income and Credit Markets

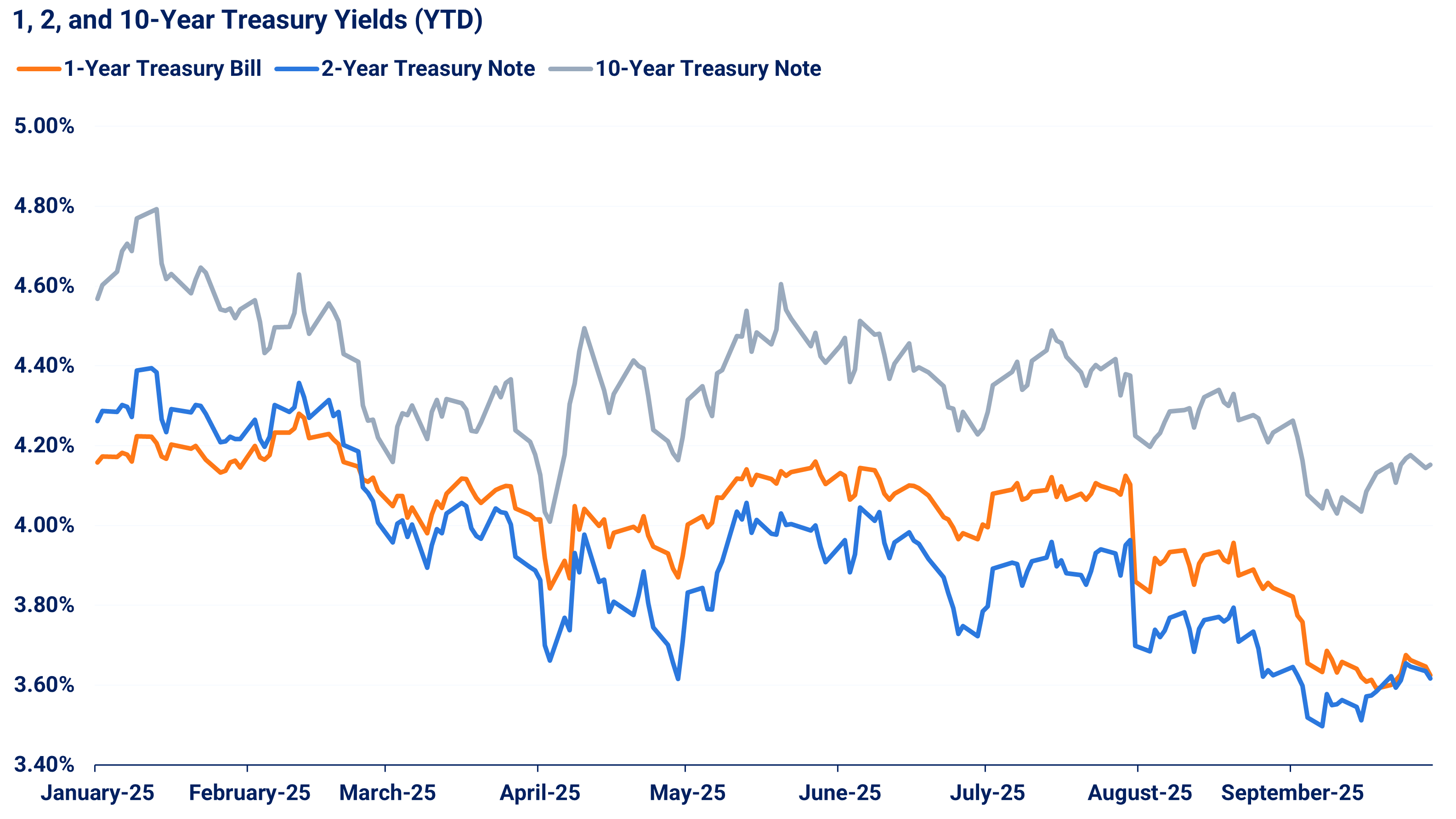

Treasury yields declined across the curve, with

1-month26

to

1-year bills27 and

30-year bonds28 each falling by over 15 basis points.

US Dollar

The U.S. dollar continues to face considerable pressure30,

weighed down by a combination of political stalemate, fiscal uncertainty, and broader economic challenges.

Analysts suggest that the recent government shutdowns could further dampen sentiment surrounding the dollar.

This political instability, alongside escalating geopolitical risks, is driving investors toward safer currencies such as the Japanese yen, Swiss franc, and euro.

Consequently, this shift toward stability is likely to exert further downward pressure on the greenback. In September, the Dollar Index (DXY) showed modest fluctuations, ultimately closing at 97.79, still reflecting a notable year-to-date decline of approximately 10%.

Sentiment

The VIX Index indicated low volatility31 fluctuating between 15 and 17 in September.

The CNN Fear and Greed Index32 fluctuated between the neutral and greed zones throughout the month (50 to 62), ultimately finishing at 50 (neutral).

ETF of the Month

Gold and silver have extended their rally, supported by the Federal Reserve’s September rate cut and expectations for two additional cuts later this year.

Year to date,

gold has advanced roughly 45%33,

while

silver has outperformed with gains of about 60%34.

Mining companies, whose performance is typically magnified relative to the underlying commodities due to operational leverage, have delivered even stronger returns.

Mining-focused ETFs, such as

VanEck Gold Miners ETF (GDX)36,

VanEck Junior Gold Miners ETF (GDXJ)37,

Global X Silver Miners ETF (SIL)38,

and

Amplify Junior Silver Miners ETF (SILJ)39 each rose more than 20% in the past month.

Imperial Fund Asset Management is a SEC-registered investment adviser.

SEC registration does not imply a certain level of skill or training.

The information provided is for informational purposes only and should not be considered investment advice or a solicitation to buy or sell any securities.

All investments involve risk, including the possible loss of principal. Please review our

full disclaimer for additional information.