In May, U.S. equities climbed to fresh record highs, though the rally masked a fractured market beneath the surface – leadership narrowed sharply into mega-cap technology,

leaving most sectors in the red. Inflation reaccelerated to its fastest pace in nearly three years, Treasury yields rose across the curve,

and the Fed completed a historic leadership transition, all while credit spreads held near cycle-tight levels and a steep oil selloff on easing Middle East

tensions reshaped the commodity landscape.

Macroeconomic Review

Inflation

Headline CPI rose 0.6% in April on a seasonally adjusted basis, lifting the annual headline rate to 3.8 percent, the highest since May 2023. Core CPI, which excludes food and energy,

rose 0.4% and 2.8%, respectively, keeping inflation well above the Federal Reserve's 2% goal.

Energy was the dominant driver. The index for energy rose 3.8 percent in April, accounting for over forty percent of the monthly all items increase, and the shelter index rose 0.6 percent.

GDP

Real U.S. gross domestic product grew at a 1.6% annualized rate in the first quarter of 2026, according to the Bureau of Economic Analysis’s second estimate.

An improvement from the 0.5% pace in the fourth quarter of 2025, though it was revised downward from the initial 2.0% advance reading.

The revision primarily reflected lower estimates for investment and consumer spending.

For the second quarter, the Atlanta Fed’s GDPNow tracking model currently projects 3.0% annualized growth as of June 1, down from a peak forecast of 4.3% on May 21.

Federal Reserve Policy

Kevin Warsh was sworn in as Chairman of the Federal Reserve on May 22, 2026, succeeding Jerome Powell. His Senate confirmation on May 13 passed by a narrow 54-45 margin,

marking one of the most divisive confirmation votes in the central bank’s history. Warsh has signaled a commitment to stricter inflation control, more streamlined communications,

and a narrower focus for the central bank, while pledging to preserve its independence.

At its late-April meeting, the FOMC kept the federal funds rate unchanged in the 3.50%–3.75% target range. Policymakers observed that economic growth remained solid, the labor market was stable,

and inflation stayed elevated, driven in part by higher global energy prices. Warsh’s first policy meeting is set for June 16–17.

Market pricing indicates a strong expectation that rates will remain on hold at that meeting. The CME FedWatch Tool showed a 96% probability of no change as of early June. At the same time,

persistent inflation and steady economic momentum have prompted some analysts to consider the possibility of rate hikes later this year rather than cuts.

Manufacturing

The ISM Manufacturing PMI registered 54 percent in May, 1.3 percentage points higher than in April and its highest reading since May 2022, with the overall economy in expansion for the 19th month in a row.

The reading marked a fifth consecutive month of expansion in the manufacturing sector.

Underlying components were firm. The New Orders Index registered 56.8 percent, up 2.7 percentage points, the Production Index rose to 54.3 percent, the Prices Index eased to 82.1 percent, a 2.5-percentage point decrease,

and the Employment Index registered 48.6 percent, up 2.2 percentage points while remaining in contraction.

The still-elevated prices reflected continued input cost pressure. Sixteen of 18 industries expanded, signaling a broadening recovery even as costs stayed high.

Labor Market

The May employment report showed a solid gain in nonfarm payrolls. Total employment rose by 172,000 in May, well above consensus expectations of around 88,000. The unemployment rate held steady at 4.3%,

in line with forecasts and remaining within the narrow 4.3%–4.5% range observed since July 2025.

Job gains were concentrated in leisure and hospitality (+70,000, including a strong +48,000 in food services and drinking places), local government (+55,000), and health care (+35,000).

Employment in financial activities declined by 22,000. The report also included notable upward revisions to prior months: March was revised higher by 29,000 to +214,000,

and April was revised up by 64,000 to +179,000, bringing the combined gain for those two months to 93,000 more than previously reported.

Cross-Asset Performance Review

Equity Markets

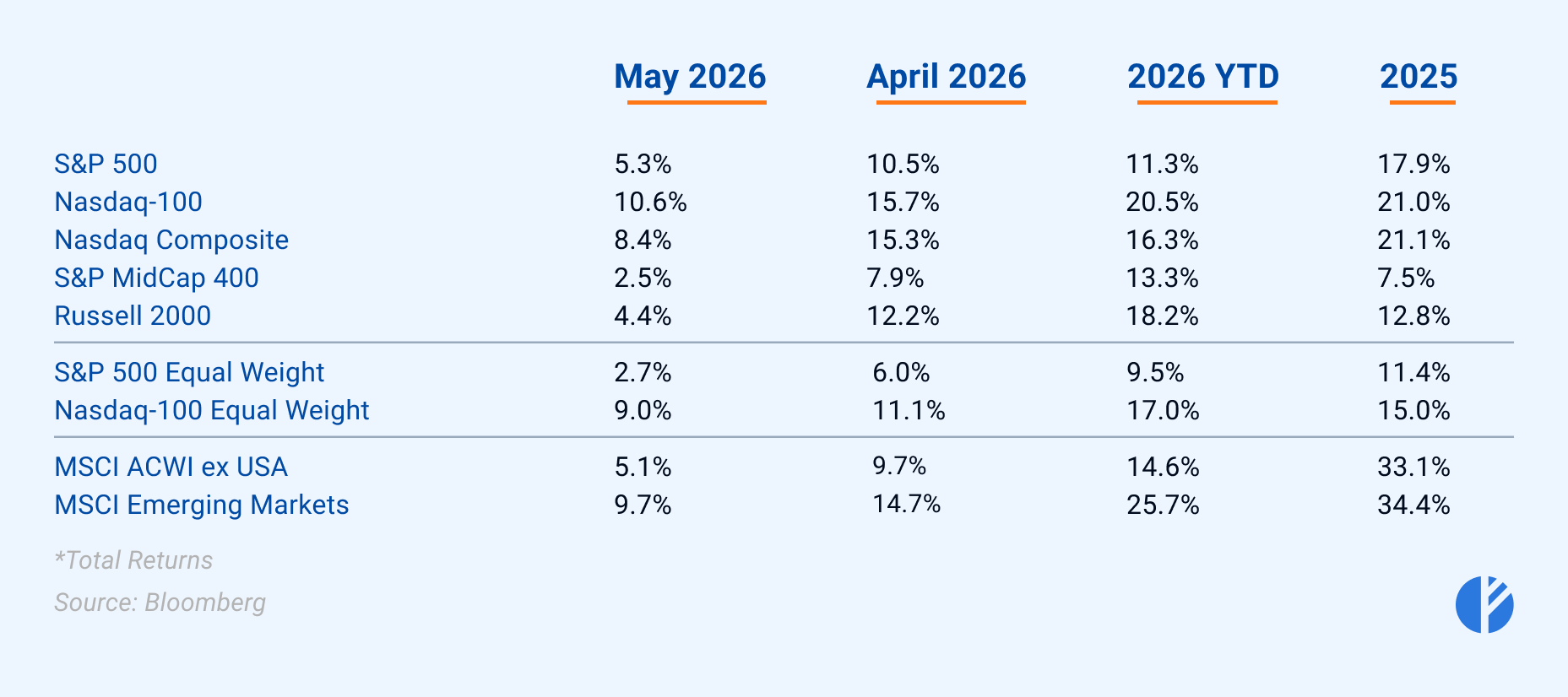

U.S. equity benchmarks posted broadly positive returns in May, led decisively by large-cap technology. The Nasdaq-100 gained 10.6% and the Nasdaq Composite rose 8.4%, outpacing the S&P 500's 5.3% advance.

Mid- and small-cap indexes comparatively lagged, with the S&P MidCap 400 up 2.5% and the Russell 2000 up 4.4%.

International markets were strong too, as the developed markets’ index returned 5.1% and the emerging markets’ one gained 9.7%.

The dispersion between capitalization-weighted and equal-weighted indexes pointed to narrow leadership. The S&P 500 Equal Weight index rose only 2.7%, trailing the cap-weighted S&P 500 by 2.6 percentage points,

a clear sign that mega-cap names drove the bulk of the gains. The Nasdaq-100 Equal Weight index advanced 9.0% versus the cap-weighted 10.6%,

a narrower but similar pattern confirming that large-cap breadth was thin even as headline indexes reached new highs.

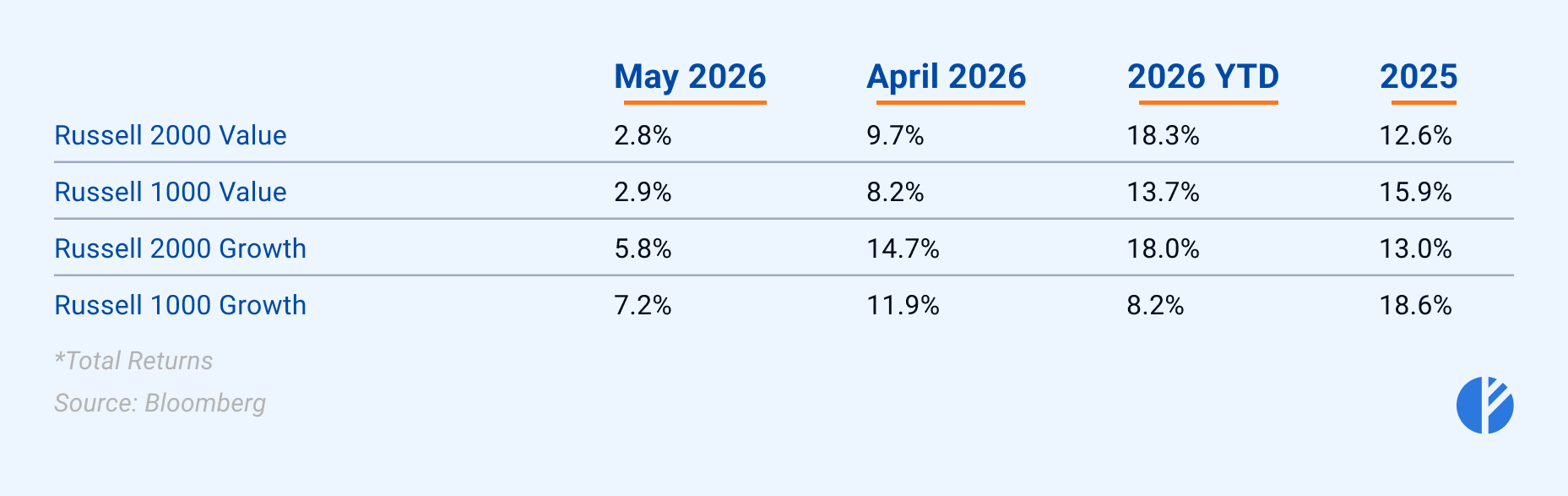

Growth outperformed value across the capitalization spectrum. The Russell 1000 Growth index rose 7.2% while the Russell 1000 Value index gained 2.9%,

a spread of more than four percentage points reflecting the dominance of technology and AI-linked names. Among smaller companies, the Russell 2000 Growth index advanced 5.8%

against the Russell 2000 Value index's 2.8%. Growth leadership was therefore pervasive at both ends of the size scale, with large-cap growth setting the overall pace.

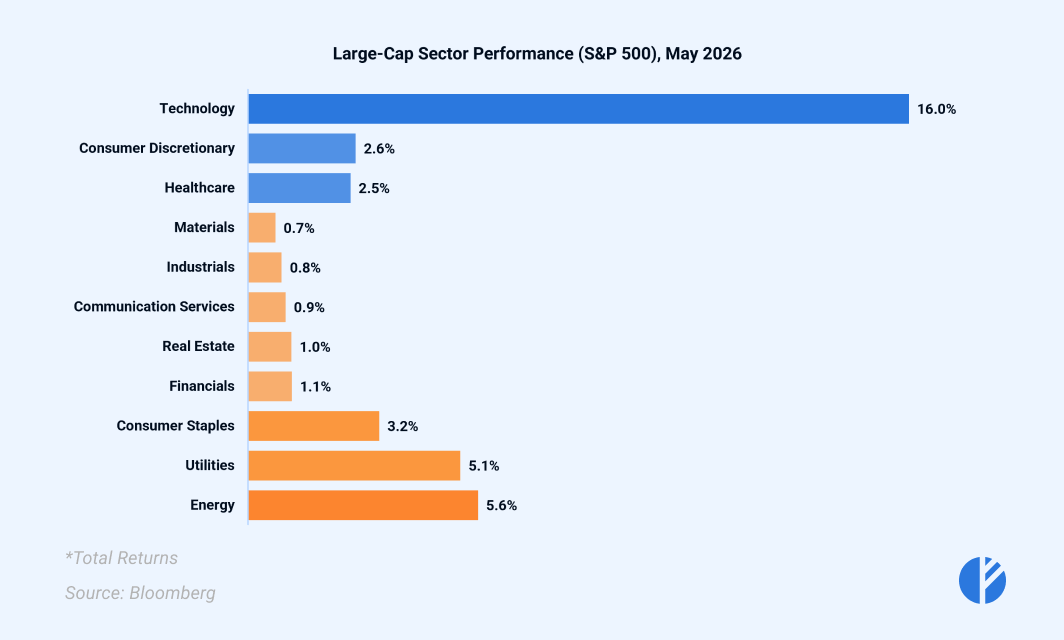

S&P 500 large-cap sector performance was extraordinarily concentrated, with eight of the eleven sectors finishing in negative territory. Technology surged 16.0%,

dwarfing every other sector and masking weaknesses elsewhere, supported by a historic surge in the semiconductor industry and continued AI-related spending.

Consumer Discretionary at 2.6% and Health Care at 2.5% were the only other gainers. The laggards clustered in rate-sensitive and commodity-linked areas,

with Energy down 5.6% as oil retreated, Utilities down 5.1%, and Consumer Staples down 3.2%. Financials fell 1.1%, Real Estate 1.0%,

Communication Services 0.9%, Industrials 0.8%, and Materials 0.7%. The thematic takeaway was unambiguous, with leadership narrowly anchored to secular growth

and most cyclical and defensive sectors lagging.

Fixed Income

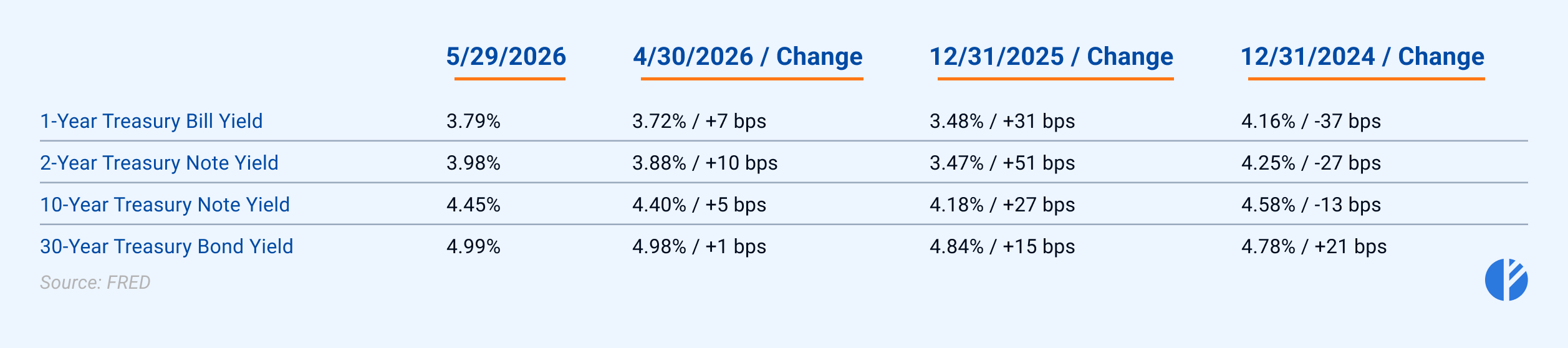

Treasury yields rose across the curve in May, extending a broader uptrend in rates and reflecting a significant repricing of Federal Reserve policy expectations.

The 1-year yield finished the month at 3.79%, up 7 basis points, while the 2-year yield rose 10 basis points to 3.98%. The 10-year yield increased 5 basis points to 4.45%,

and the 30-year yield edged up 1 basis point to 4.99%.

On a year-to-date basis, the moves were more pronounced, with the 2-year yield up 51 basis points and the 1-year yield up 31 basis points since the end of 2025.

This shift indicates that markets have largely priced out near-term rate cuts for 2026 – previously anticipating as many as three 25-basis-point easings – with some

futures now embedding modest hike probabilities later in the year or into 2027.

The primary drivers are sticky inflation and a resilient labor market. Additional upward pressure emerged mid-month from geopolitical tensions related to Iran,

which drove oil prices sharply higher and briefly pushed the 30-year yield above 5.18%, its highest level since before the 2008 financial crisis. Yields later retraced

modestly as oil prices eased on hopes of de-escalation, but the net increase in real rates and term premium remained intact. Overall, the flattening bias aligns with expectations

of a more restrictive or “higher-for-longer” policy stance rather than aggressive monetary easing.

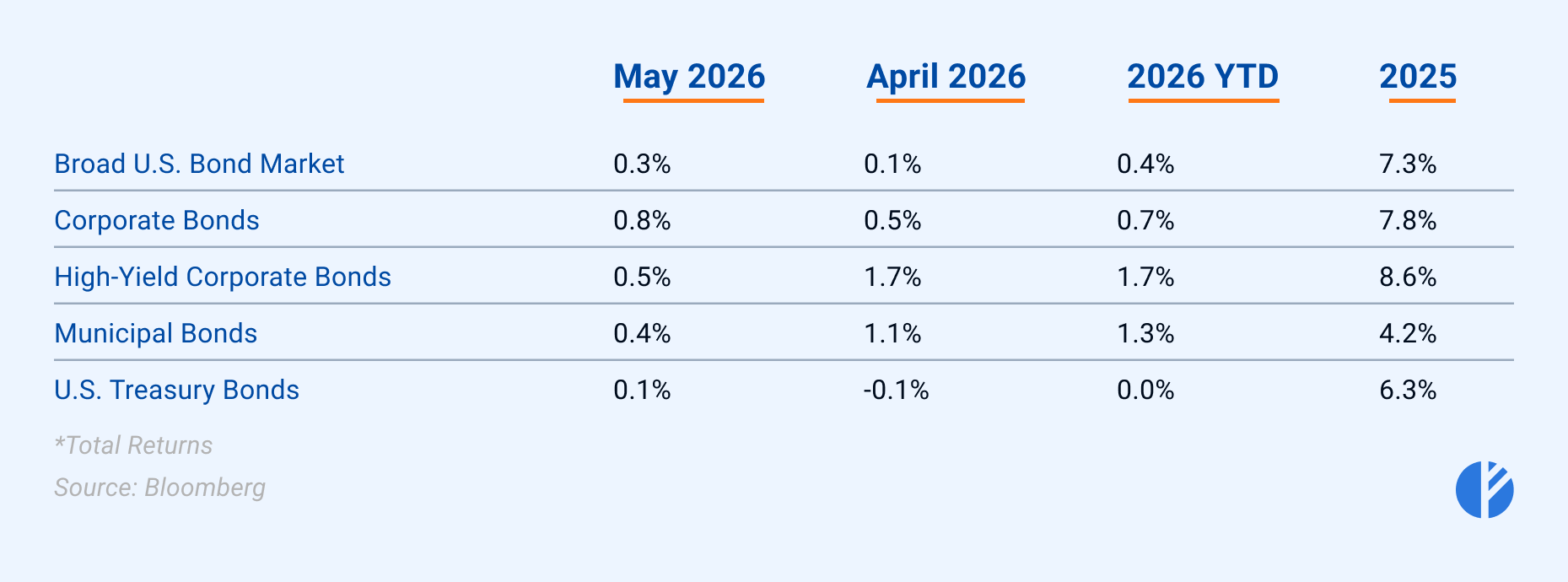

Bond index returns were modestly positive across most segments. The broad U.S. bond market returned 0.3%, while corporate bonds led with a 0.8% gain.

High-yield corporate bonds returned 0.5%, a marked deceleration from April's 1.7% advance, and municipal bonds added 0.4%. U.S. Treasury bonds were the weakest segment at 0.1%,

leaving them flat year-to-date at 0.0% as rising yields offset coupon income. The outperformance of corporate credit over Treasuries reflected the firm risk appetite that

characterized the month.

Credit spreads remained near historically tight levels, consistent with the risk-on tone in equities. The option-adjusted spread on the investment-grade corporate bonds

decreased even further down from 0.81% to 0.74%, while the high-yield option-adjusted spread fluctuated around 2.70–2.80% percent throughout the month.

Commodities

Oil prices declined sharply in May. WTI crude futures fell approximately 19–20% for the month – its weakest performance since April 2025 – settling near $87.36 per barrel.

Brent crude futures dropped more than 19%, marking its largest monthly decline since March 2020.

The selloff was primarily driven by growing optimism around a potential U.S.-Iran ceasefire. Late in the month, negotiators reached a tentative 60-day memorandum of

understanding to extend the existing ceasefire and initiate talks on Iran’s nuclear program. This development significantly reduced the geopolitical risk premium that had

supported prices earlier in the year amid tensions over the Strait of Hormuz. Additional downward pressure came from OPEC+ maintaining output discipline and a broader recalibration

of supply concerns.

Precious metals showed signs of stabilization following steep declines from their February 2026 highs. In May, gold declined modestly by 1.7%, while silver posted a slight gain

of 2.1%.

The divergence reflects contrasting fundamental drivers. Silver continues to benefit from expectations for sustained industrial demand, particularly in solar energy,

electric vehicles, and electronics. Gold, by contrast, remains sensitive to higher real yields and a firmer U.S. dollar, which tempered its appeal as a safe-haven asset.

This article draws on data and insights from the U.S. Bureau of Labor Statistics (BLS), the United States Joint Economic Committee, the Institute for Supply Management (ISM),

the Federal Reserve Bank of Atlanta, Bloomberg, and FRED (Federal Reserve Economic Data), as well as leading financial publications including CNBC, MarketWatch, and Nasdaq.