In October, financial markets navigated heightened volatility amid a prolonged U.S. government shutdown, renewed U.S.–China trade tensions, and shifting monetary policy expectations.

Despite the turbulent backdrop, equities ended the month higher, supported by optimism following the late-month Trump–Xi talks in Busan.

The Federal Reserve delivered a 25-basis-point rate cut to a range of 3.75%–4.00%, though Chair Powell signaled uncertainty about further easing in December.

Major headlines

Government shutdown

Fed Cuts Rates to 3.75%–4.00%

In the post-meeting statement, Chair Jerome Powell emphasized that it remains uncertain whether another rate cut will follow in December, citing limited visibility on key economic indicators due to the ongoing government shutdown.

Following the announcement,

futures markets corrected their expectations6,

with the probability of a December cut falling from 85% before the meeting to 62% afterward.

U.S. national debt hits $38 trillion

The United States’ gross national debt surpassed a historic milestone of $38 trillion7,

just two months after crossing the $37 trillion mark—marking the fastest non-pandemic-era increase of one trillion dollars in U.S. history.

According to the Joint Economic Committee,

the national debt has been expanding at a pace of nearly $70,000 per second over the past year8.

Fiscal experts warn that the surging debt is fueling higher interest expenses9,

now the fastest-growing component of the federal budget.

As Michael Peterson noted, while the U.S. spent about $4 trillion on interest payments over the past decade, it is now projected to spend $14 trillion over the next ten years, underscoring the growing strain on federal finances.

New Phase in U.S.–China Talks

A new chapter in U.S.–China relations unfolded this month. On October 10,

President Donald Trump announced plans to impose a 100 percent tariff on Chinese goods11 beginning November 1,

alongside new export controls on critical software.

The decision followed

Beijing’s earlier move to restrict exports of rare earth magnets and raw materials12.

In response,

China introduced port fees on U.S. vessels13 effective October 14—the same day Washington was set to apply similar charges on Chinese ships.

The summit produced a breakthrough, the United States agreed to reduce tariffs on Chinese goods from 57 percent to 47 percent,

while China pledged to suspend its rare-earth export controls for one year and to significant purchases of U.S. agricultural products.

Both sides also committed to closer cooperation on fentanyl trafficking prevention, economic and security dialogues, and new energy trade, including Chinese purchases of Alaskan oil and gas.

The two countries also signaled intent to resolve the TikTok dispute,

explore chip-sector engagement with Nvidia, and expand collaboration on artificial intelligence,

infectious-disease control, telecom fraud, money laundering, and illegal-immigration prevention.

Macroeconomic Review

GDP

The first estimate for U.S. GDP growth in the third quarter, originally scheduled for release on October 30,

was delayed due to the ongoing government shutdown16.

Federal Reserve Policy

Following the FOMC meeting on 29th of October,

the Federal Reserve rate was cut by 25 bps19 down to 3.75%–4.00%.

Inflation

The September CPI, released on October 24, is the only official economic data currently available due to the ongoing government shutdown.

Headline inflation rose 3.0% year-over -year20,

slightly above August’s 2.9% but below economists’ expectations of 3.1%.

Meanwhile,

core CPI also came in at 3.0%21,

easing from 3.1% in August and undershooting the 3.1% consensus forecast.

Manufacturing

U.S. manufacturing activity declined more sharply in October22,

with the ISM Manufacturing Index falling to 48.7%, down from 49.1% in September.

However, the broader U.S. economy continued to expand for the 66th consecutive month.

All four demand-related indicators showed modest improvement, though they remained in contraction territory. The Customers’ Inventories Index continued to signal “too low” inventory levels, which is typically a positive sign for future production.

On the output side, production weakened, while employment continued to contract but at a slower pace, reflecting ongoing caution among manufacturers, with most firms still focused on controlling headcount rather than hiring.

Among input measures, trends were mixed: supplier deliveries slowed further, inventories declined more quickly, and prices rose again though at a more moderate rate. Imports also remained subdued but contracted at a slower pace.

Index highlights:

- New Orders contracted for the second month in a row at 49.4% (up from 48.9%).

- Production fell back into contraction at 48.2% (down from 51.0%).

- Employment ticked slightly higher to 46.0% (from 45.3%) but remained in contraction for a ninth consecutive month.

- Supplier Deliveries slowed further to 54.2% (up from 52.6%).

- Inventories declined to 45.8% (from 47.7%).

- Customers’ Inventories remained “too low” at 43.9% (slightly up from 43.7%).

- Prices stayed in expansion territory at 58.0% (down from 61.9%).

- Backlog of Orders increased modestly to 47.9% (from 46.2%).

- New Export Orders contracted for the eighth consecutive month at 44.5% (up from 43.0%).

- Imports stayed in contraction at 45.4% (up from 44.7%).

Labor Market

With the Bureau of Labor Statistics unable to publish new data due to the ongoing government shutdown, the U.S. economy is operating without an official read on October’s employment situation.

Cross-Asset Performance Review

Equity Market Performance

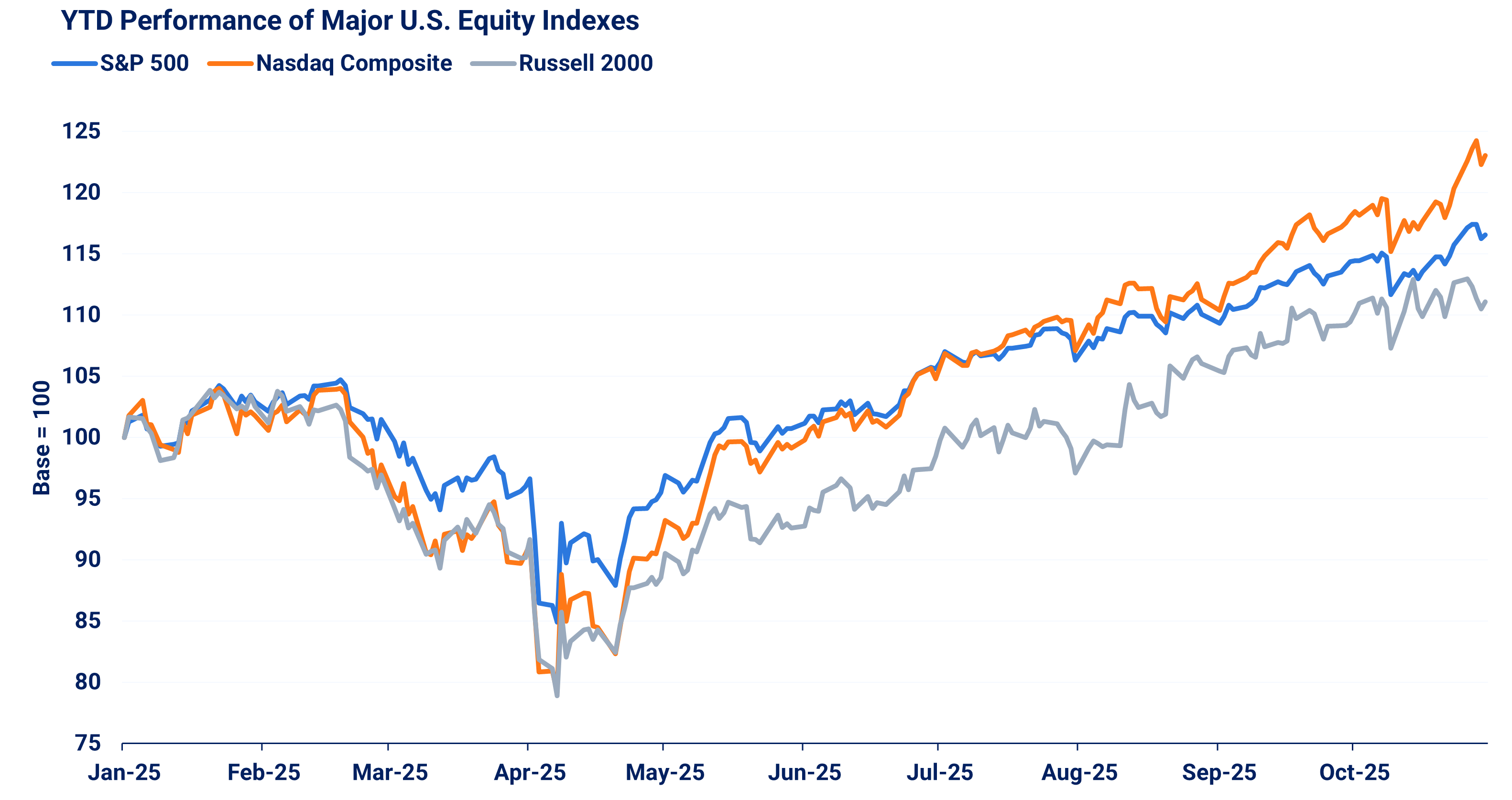

U.S. equities advanced, the tech-heavy

Nasdaq Composite26 gained 4.7% for the month,

outpacing the

S&P 50027 and

Russell 200028, which rose 2.3% and 1.8%, respectively.

Global markets also rose, with the

MSCI World ex U.S. index29 adding 1.1%.

Noteworthy, mid-month volatility emerged as renewed U.S.–China tensions briefly rattled markets, sending major U.S. indexes down 3–4% on October 10.

However, sentiment quickly improved as both sides initiated de-escalation talks, allowing equities to recover and end the month higher.

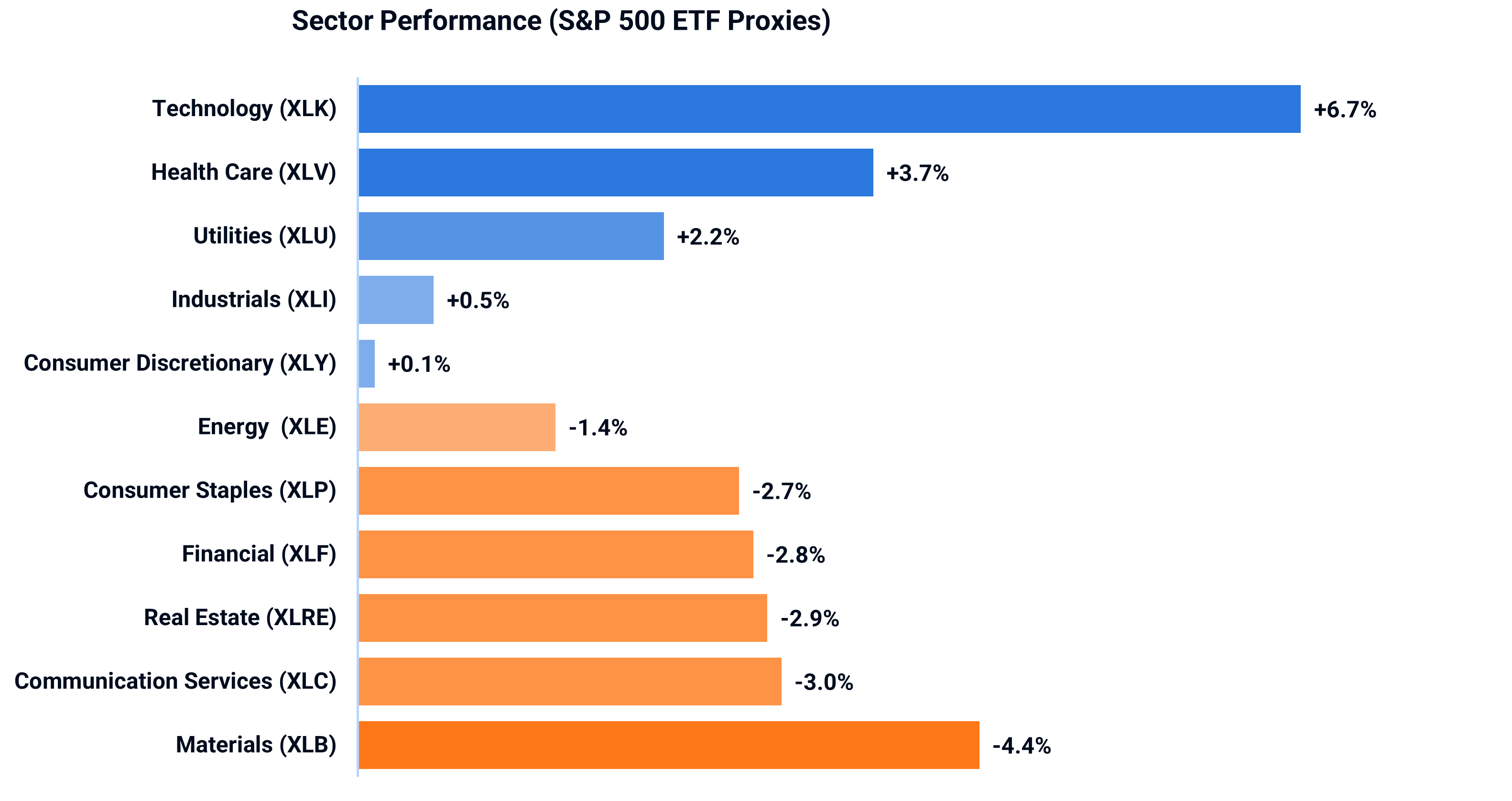

Sector Highlights

The technology sector, proxied by the Technology Select Sector SPDR Fund (

XLK30),

continued to lead the market’s advance adding up 6.7% in October,

surging more than 40% since May—its strongest six-month performance since 202031.

Healthcare (

XLV32) also posted solid gains of 3.7%,

while Utilities (

XLU33) advanced 2.2%.

Industrials (

XLI34)

and Consumer Discretionary (

XLY35) registered modest gains of 0.5% and 0.1%, respectively.

On the other hand, Materials (

XLB36) led the laggards with a 4.4% decline.

Communication Services (

XLC37) fell 3.0%,

while Real Estate (

XLRE38) declined 2.9%.

Financials (

XLF39)

and Consumer Staples (

XLP40) slipped 2.8% and 2.7%, respectively.

Energy (

XLE41) posted a milder loss of 1.4%.

Fixed Income and Credit Markets

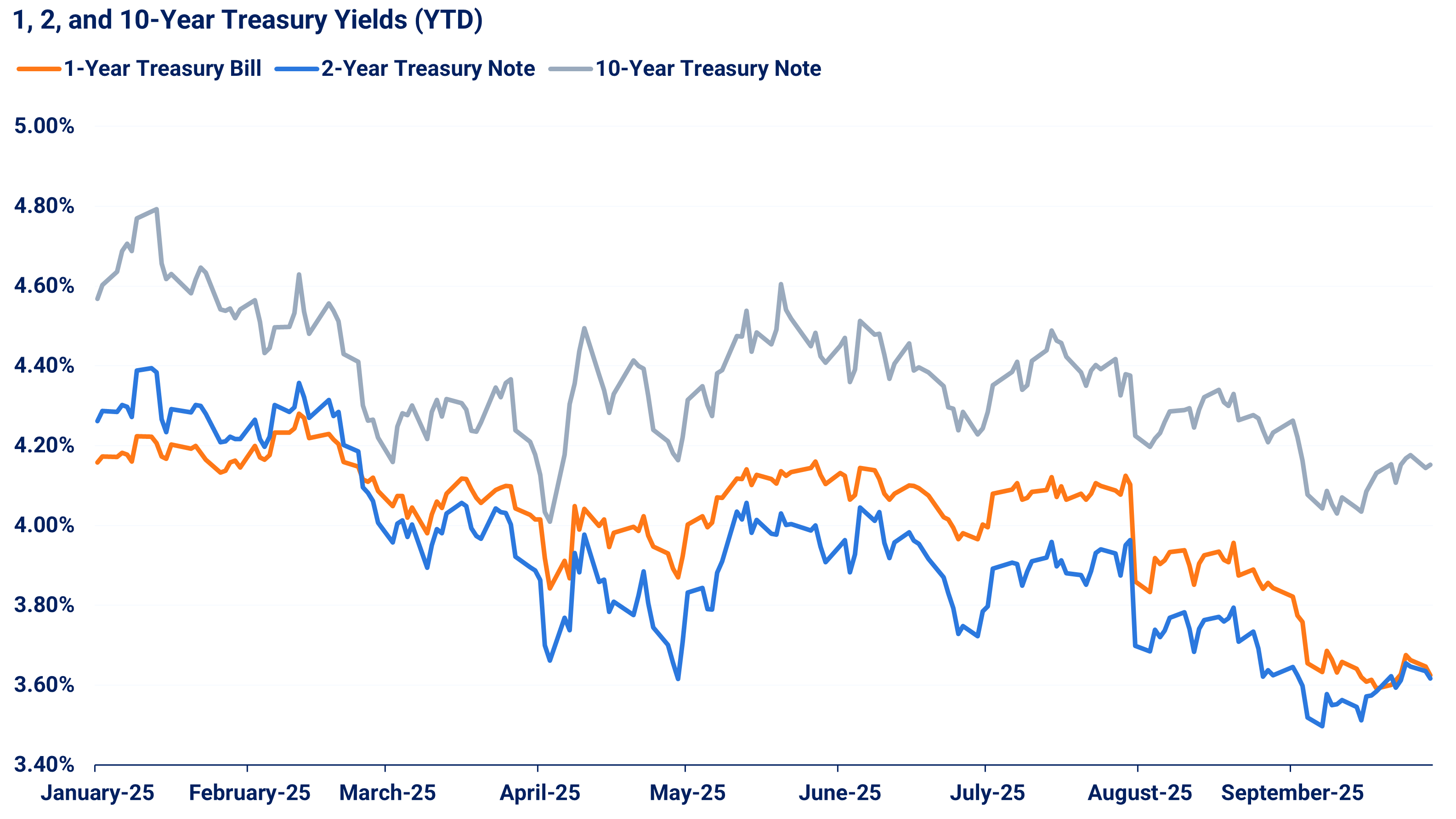

U.S. Treasury yields were decreasing through most of October reflecting market expectations for continuing easing.

At their monthly lows,

the one-year Treasury bill yield had fallen by 8 basis points42,

the two-year note by 19 basis points43,

and

the ten-year note by 20 basis points44.

However, following Chair Jerome Powell’s remarks suggesting that a December rate cut was not yet assured, yields rebounded, with the listed maturities each rising by roughly 10 basis points.

The spread between U.S. investment-grade corporate bonds and risk-free Treasury yields widened slightly mid-month45

amid uncertainty stemming from U.S.–China tensions, but remained relatively tight, fluctuating between 0.74% and 0.81%.

US Dollar

After a difficult start to 2025—the dollar’s weakest first half since the early 1970s—

the U.S. dollar has staged a steady recovery46

since the Federal Reserve began cutting interest rates in September. Expectations of further weakness faded as policymakers adopted a more cautious stance, providing support for the greenback.

The rebound has also been driven by softness in major counterparts, with Europe struggling amid sluggish growth and Japan’s renewed fiscal stimulus pressuring the yen.

Precious metals

Gold48 and

Silver49 extended their gains in October amid heightened geopolitical tensions and market volatility.

Gold climbed to a new all-time high of $4,381 per ounce on October 2050

before easing to $4,002 by month-end, still up more than 3% month-on-month.

Silver followed a similar trajectory, surging nearly 16% mid-month before paring gains to close 3.8% higher.

Analysts note that the mid-month peaks in both metals were largely driven by escalating geopolitical risks51,

which intensified safe-haven demand in an already overheated market.

Crude Oil

West Texas Intermediate (WTI) crude experienced notable volatility, reflecting shifting global dynamics in both demand and supply.

Mid-month,

prices plunged52

by as much as 8%53 from early October levels as renewed trade war risks rattled markets and reignited fears of slowing global growth.

Toward the end of the month, WTI eased slightly as investors reassessed the long-term impact of the sanctions and weighed them against signals of possible production increases from OPEC+, reflecting growing uncertainty about future supply dynamics.

Ultimately, the index declined by 2.4%, slipping from $62.67 to $61.15 per barrel over the month.

Cryptocurrencies

Cryptocurrencies retreated55,

with both Bitcoin and Ethereum posting notable declines amid renewed market volatility.

The sharpest losses occurred on October 10,

when escalating U.S.–China trade tensions triggered a broad risk-off move across global markets56—sending

Bitcoin down 7%57 and

Ethereum plunging 12%58 in a single day.

Overall, Bitcoin fell around 4% over the month, while Ethereum dropped roughly 7%.

Sentiment

In October, market volatility ticked higher compared to the previous months, with the

VIX peaking at 25.359 amid renewed geopolitical and financial tensions.

The index recorded its largest single-day surge in more than six months on October 10, climbing to 21.6 as U.S.–China tensions unsettled investors.

Volatility spiked further on October 1760,

reaching 25.3 following reports of

loan defaults at regional lenders Zions Bancorporation and Western Alliance Bancorp61.

However, sentiment improved toward month-end on as investors saw that the loan-default effects of the banks were isolated, solid Q3 reports of the S&P 500 companies, and the meeting between the U.S.

and Chinese leaders relations, bringing the VIX back down to its recent comfort zone near 15–17.

Amid heightened uncertainty throughout October,

the Fear and Greed Index swung sharply between 23 (Extreme Fear) and 57 (Greed)62,

spending nearly two-thirds of the month in fear or extreme fear territory.

The index ultimately ended the month at 48 (Neutral), supported by a late-month rebound in sentiment following the positive outcome of the Trump–Xi meeting.

ETFs of the Month

South Korea

South Korea’s equity market soared to record highs in October63,

with

the benchmark KOSPI index surging 20% in a single month64.

The rally was powered by the country’s semiconductor giants,

Samsung Electronics65 and

SK Hynix66,

which gained 28% and an astonishing 60%, respectively, as investors continued to bet on the global artificial intelligence boom.

Several macro tailwinds reinforced the momentum, including a more dovish monetary outlook from the Bank of Korea, a new trade agreement with the United States, and sustained optimism around AI-driven growth.

Biotech

Biotech stocks are staging a strong comeback after several years of underperformance68.

The SPDR S&P Biotech ETF (XBI) has gained 25% year-to-date through October 31, outperforming the S&P 500 by about nine percentage points.

The sector’s rally has been fueled, among other factors, by successful drug trials and new product launches, increased merger and acquisition activity, and declining interest rates, which have lowered financing costs for research-intensive firms and lifted valuations through reduced discount rates.

Reflecting renewed investor confidence, biotech ETFs such as the

SPDR S&P Biotech ETF (XBI)69 and the

iShares Biotechnology ETF (IBB)70 advanced more than 10% in October.

Argentina

Argentina’s markets surged in October following President Javier Milei’s party’s sweeping victory in the midterm elections71.

The results secured Milei a veto-proof majority in Congress, bolstering confidence that his administration will be able to advance its ambitious reform agenda.

Argentine equities and the peso rallied sharply in October, with the country’s main index,

the MERVAL, surging nearly 70% during the month72.

The rally reflected investor optimism over expectations of continued market-friendly reforms, including privatizations, fiscal consolidation, and deregulation aimed at stabilizing the economy and curbing inflation.

The Global X MSCI Argentina ETF (ARGT), directly targeting Argentine stocks

surged over 35%73.