In November, markets digested the economic fallout from the record 43-day U.S. government shutdown. Investors spent much of the month focused on the December Fed meeting.

U.S. equities were volatile but ultimately mixed amid mounting concerns over a potential AI bubble.

Defensive sectors such as healthcare and consumer staples outperformed, buoyed by relative value, deal activity, and a rotation away from richly valued tech, while strong gains in precious metals and natural gas supported materials and energy.

Major Headlines

Record Shutdown Ends

On November 12, the longest in U.S. history,

43-day federal government shutdown ended1, when Congress narrowly approved and President Donald Trump signed a funding bill to reopen agencies after a failure to approve funding that began on October 1.

The shutdown furloughed roughly 900,000 federal workers, forced millions more to work without pay,

and disrupted essential services ranging from food assistance to air-traffic control and national park operations,

ultimately leaving an estimated $11 billion in permanent economic damage.2

The House passed the bill by a tight 222–209 margin after Senate approval, restoring pay and benefits and extending agency funding through January 2026.

While the agreement clears a path for critical services to recover ahead of the busy Thanksgiving travel season and reinstates key economic data releases that had left markets and policymakers operating in the dark,

t does little to alter the nation’s fiscal trajectory: the government remains on pace to add about $1.8 trillion annually to its $38 trillion debt.

Macroeconomic Review

GDP

The long-postponed first revision of U.S. Q3 GDP – delayed due to the government shutdown – is now

scheduled for release on December 233.

According to the Atlanta Fed’s GDPNow model,

third-quarter GDP growth is estimated at 3.8% year-over-year4, matching

the 3.8% expansion recorded in Q2 20255.

Federal Reserve Policy

Throughout November, the Federal Reserve's key interest rate remained in the 3.75% - 4.00% range, as no meeting took place during the month. However,

much of the market’s focus centered on the anticipated December Fed meeting6.

Initially, investors were largely confident in an imminent rate cut, but this sentiment quickly shifted.

The delay in the release of October's Consumer Price Index (CPI) data, coupled with the mixed messages from the October Fed meeting about future rate cuts, led to a sharp decline in expectations for a reduction.

A significant shift in the outlook occurred with the release of the September Labor Market report, which revealed the highest unemployment rate since 2021.

This data reignited expectations for a rate cut, and by the end of the month, the likelihood of a 25 basis point reduction in December had surged, with the CME FedWatch tool assigning an 88% probability to the move.

The shift was further reinforced by the September PCE report7, published on December 5th, which showed that prices had remained relatively stable.

This stability eased concerns that a rate cut would exacerbate inflationary pressures, adding further support to the case for a December reduction.

Despite the rising expectations for a December cut, the situation remained far from certain. Federal Reserve Chair Jerome Powell and other members of the Federal Open Market Committee (FOMC) made it clear that a rate cut was not a “foregone conclusion.”

On December 10th, following the Federal Reserve meeting,

the Fed Funds rate was lowered by 25 basis points9,

bringing it to a new range of 3.50% – 3.75%, its lowest since November 2022.

Inflation

On December 5th,

the delayed September PCE data was released10, showing that the Core PCE rose by 2.8% year-over-year, slightly down from 2.9% in August and in line with expectations.

The headline PCE also came in at 2.8%, matching forecasts and edging up from August’s 2.7%. The report indicates that prices have remained relatively stable despite ongoing tariffs and robust consumer spending.

Manufacturing

Two of the four key indicators, the Backlog of Orders and New Orders, showed declines, outweighing the gains posted by the New Export Orders and Customers' Inventories indexes.

Notably, the Customers' Inventories Index contracted at a slower pace, and a "too low" status for this index is generally viewed as a positive sign for future production.

Output experienced a notable jump into expansion. However, employment trends were less favorable, as 67% of panelists (unchanged from October) reported that managing headcount continues to be the norm at their companies, rather than adding new hires.

Input indicators presented a mixed picture. The Supplier Deliveries Index showed faster deliveries, while the Inventories Index contracted at a slower rate. Meanwhile, the Prices Index continued to reflect rising costs, and the Imports Index also contracted at a slower rate.

- New Orders contracted for the third month in a row at 47.4% (down from 49.4% in October).

- Production emerged from contraction and rose to 51.4% (up from 48.2%).

- Employment fell to 44.0% (from 46.0%), remaining in contraction for the tenth month.

- Supplier Deliveries got faster with a rate of 49.3% (up from 54.2%).

- Inventories contracted at a slower rate with 48.9% (up from 45.8%).

- Customers' Inventories remained "too low" at 44.7% (slightly up from 43.9%).

- Prices stayed in expansion territory at 58.5% (down from 58.0%).

- Backlog of Orders increased modestly to 44.0% (from 47.9%).

- New Export Orders contracted for the eighth consecutive month at 46.2% (up from 44.5%).

- Imports stayed in contraction at 48.9% (up from 45.4%).

Labor Market

The Bureau of Labor Statistics is scheduled to

release the combined October–November Jobs Report on December 1613.

Until then, the most recent available data is the September Jobs Report, published on November 20.

According to that report,

the U.S. economy added 119,000 jobs in September14,

more than doubling the consensus forecast of 50,00015.

However, the unemployment rate rose for the third straight month, reaching 4.4%, its highest level since early 2021.

Cross-Asset Performance Review

Equity Market Performance

November proved notably volatile for U.S. equities.

The S&P 50016,

Nasdaq Composite17, and

Russell 200018

spent most of the month under pressure, reaching their monthly lows on November 20th, with the S&P 500 down 4.4% from October’s close,

the Nasdaq lower by 6.9%, and the Russell 2000 off 7.1%. Investor sentiment weakened ahead of NVIDIA’s closely watched earnings release, as

worries about an emerging AI bubble and stretched valuations in artificial intelligence–focused stocks mounted19.

NVIDIA, however, beat expectations –

reporting EPS of $1.30 versus the forecasted $1.2620 – underscoring persistent demand for AI chips and helping to calm market concerns.

Coupled with renewed optimism around potential December rate cuts, the results triggered a sharp rebound, with major indexes rallying 5–8% over the subsequent eight days.

By month-end, the S&P 500 managed a modest 0.1% gain, the Nasdaq finished down 1.5%, and the Russell 2000 closed with a 0.9% increase.

The healthcare sector experienced a substantial rally21, with the

XLV rising over 9%22.

Several factors contributed to this surge, including comparatively cheaper valuations, growing expectations for rate cuts, positive FDA approvals, and strong deal activity.

Additionally, as concerns about the AI bubble mounted, many investors rotated into safer sectors, with healthcare emerging as a preferred choice.

Fueled by this growth, Eli Lilly briefly crossed the $1 trillion market cap, becoming the first-ever healthcare company to reach this remarkable milestone.

Another defensive sector, consumer staples, also saw heightened demand amid AI-related concerns.

Its proxy,

XLP, gained over 4%23. Meanwhile, the continued rally in gold and silver provided significant support for the materials sector (

XLB24).

Similarly, the exceptional rise in natural gas prices served as a strong tailwind for the energy sector (

XLE25).

The real estate sector (

XLRE26) posted a modest increase of 1.9%,

the financial sector (

XLF27) gained 1.8%.

Utilities (

XLU28) also saw a rise of 1.7%

and communication services (

XLC29) recorded a more subdued gain of 0.5%.

On the other hand, the industrial sector (

XLI30) saw a slight decline of 0.9%,

and consumer discretionary (

XLY31) faced a dip of 1.4%.

The technology sector (XLK) experienced the largest decline, falling 4.8%.

This drop was largely driven by growing worries over the potential AI bubble32,

prompting investor caution and a shift away from technology stocks.

Fixed Income and Credit Markets

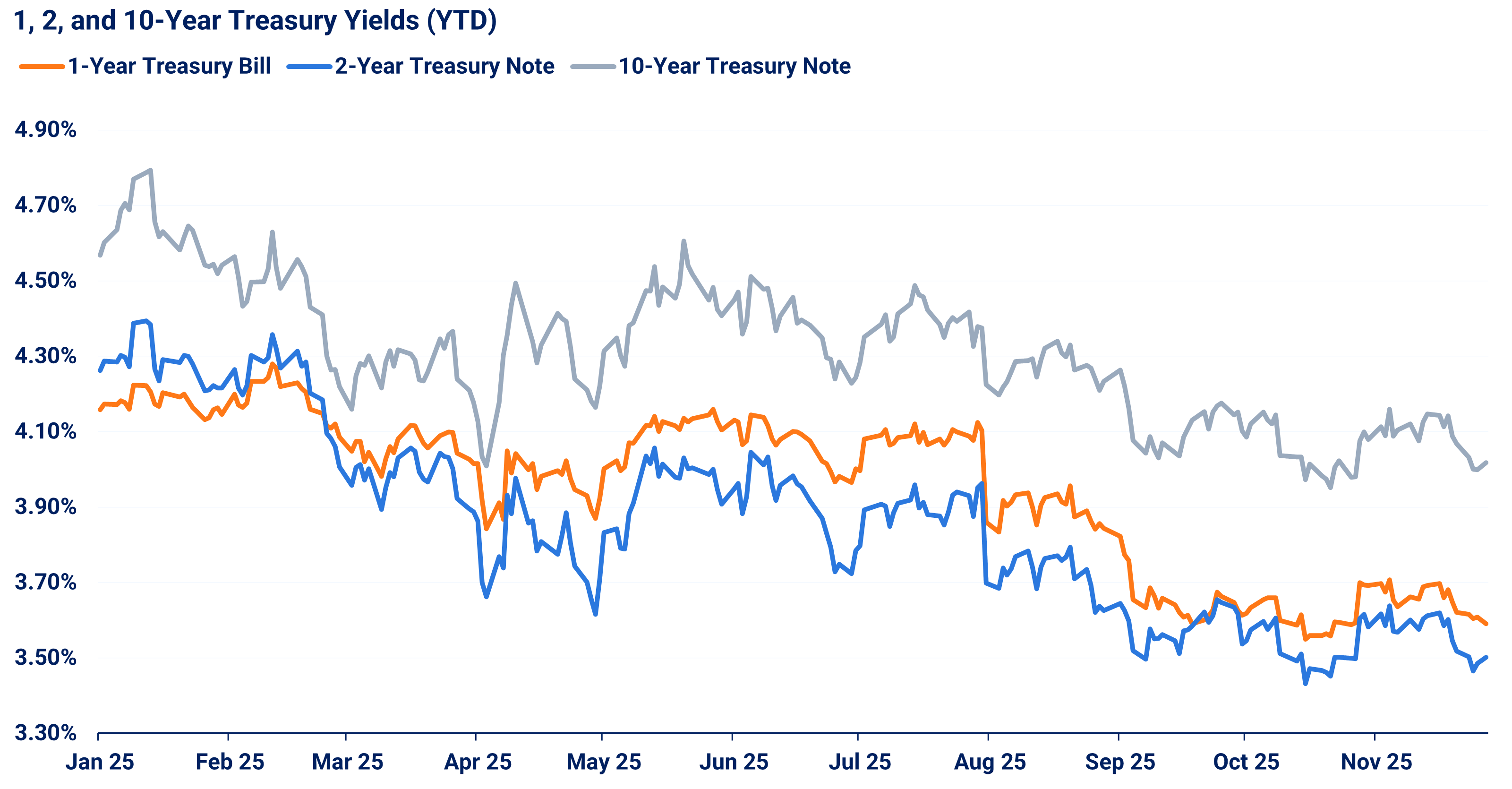

Yields on

1-33,

2-34,

and

10-year U.S35.

Treasuries declined in November, reflecting growing investor expectations for Federal Reserve rate cuts. Over the month, the one-year Treasury yield fell by 10 basis points, the two-year by 8 basis points, and the ten-year by 6 basis points.

The spread between U.S. investment-grade corporate bonds and risk-free Treasury yields remained relatively tight,

fluctuating between 0.80% and 0.86%.36

US Dollar

The U.S. dollar experienced some volatility throughout the month,

driven by uncertainty surrounding the upcoming December rate decision37.

However, it ultimately ended the month nearly flat,

with a slight decrease of 0.2%38, closing at a DXY of 99.5.

Precious metals

Gold continued its upward trend, though at a slower pace compared to previous months,

gaining approximately 5% during the month39 and surpassing $4,200 per ounce again.

Meanwhile, silver saw a remarkable rally,

increasing by over 16%40 and reaching $56 per ounce.

Crude Oil

Natural Gas

Cryptocurrencies

Cryptocurrencies faced significant declines,

with

Bitcoin experiencing a drop of over 17%45,

falling to $90,369 and

Ethereum declining by 22%46 to reach $2,991.

This marks the largest downturn since 2021, driven by market conditions that have led investors to adopt a more cautious approach.

Sentiment

The VIX index remained relatively moderate throughout the month47,

although surpassing 20 and spiking up to 26 mid-month driven by

concerns48

about overheated tech valuations and uncertain monetary policy, and mixed labor market signals.

These pressures were also reflected in the CNN Fear & Greed Index49, which dropped below 10, signaling extreme fear for the first time since the tariff shock in April.

ETFs of the Month

Natural Gas

U.S. natural gas prices surged50, jumping more than 13%

to reach a three-year high. The most significant driver has been an unprecedented wave of LNG exports51.

Shipments exceeded 10.1 million tons in October – marking the first time any country has crossed the 10-million-ton threshold in a single month – and climbed even higher to 10.9 million tons in November.

This surge in outbound demand has meaningfully tightened the domestic supply-demand balance just as winter heating requirements ramp up.

Colder-than-expected early winter temperatures across the Northern Hemisphere accelerated inventory drawdowns, adding further pressure.

By late November, U.S. utilities withdrew substantially more gas from storage than anticipated, signaling heightened urgency to replenish inventories heading into peak winter demand.

Beyond export strength and weather-driven consumption, structural demand from the power sector is emerging as a powerful new force in the natural gas market. Electricity usage from AI-driven data centers continues to grow at double-digit rates. With natural gas fueling more than 40% of U.S. power generation the AI boom is becoming an increasingly important pillar of long-term gas demand.

Reflecting these market forces, the

United States Natural Gas Fund ETF (UNG)52 – which tracks front-month natural gas futures – rose more than 11% over the month.

Silver

Healthcare

Healthcare stocks have significantly outperformed the broader market58, as rising concerns about a potential AI bubble weighed on tech and encouraged investors to rotate into more defensive areas of the market.

Reflecting this shift, healthcare-focused ETFs across pharmaceuticals, biotechnology, and broad healthcare delivered strong gains in November.

VanEck Pharmaceutical (PPH)59,

iShares U.S. Healthcare (IYH)60,

iShares Biotechnology (IBB)61 and

SPDR S&P Biotech (XBI)62 each advanced close to 9–10%.