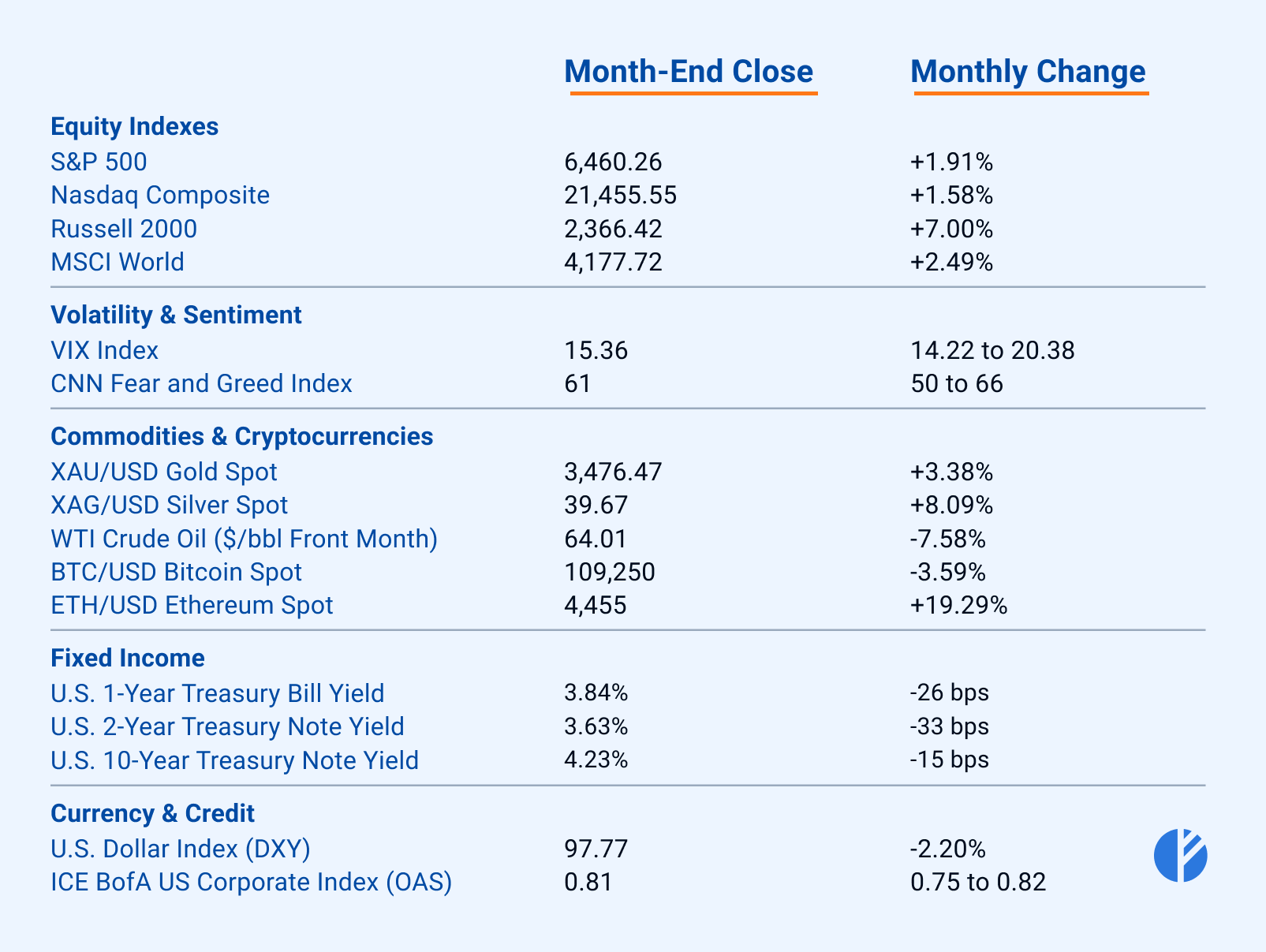

In August, financial markets navigated a wave of renewed U.S. tariff actions, growing expectations of monetary easing, and mixed economic data.

Equities rallied broadly, driven by small caps and cyclical sectors, even as manufacturing stayed in contraction and job growth slowed.

Meanwhile, Treasury yields slipped and the dollar weakened, underscoring mounting bets that monetary easing appears imminent.

Major Headlines

Tariff Increases

On August 7,

President Trump enacted a sweeping new wave of tariffs affecting 69 trading partners1.

Previously, nearly all imports faced a uniform 10% duty, but rates now vary widely by country.

The steepest tariffs include 50% on Brazil and India, 40% on Laos and Myanmar, 39% on Switzerland, and 35% on Iraq and Serbia.

In total, 21 additional countries now face levies above 15%, among them key U.S. suppliers such as Vietnam, India, Taiwan, and Thailand.

Meanwhile, 39 countries plus the European Union are subject to a 15% tariff.

S&P Affirms U.S. Credit Rating

S&P Global reaffirmed the U.S. credit rating at AA+/A-1+2,

citing that surging tariff revenues (up 242 % YoY, $30B in July) will help offset deficits from the One Big Beautiful Bill Act tax cuts.

The agency noted the U.S.’s resilient, diversified economy with per-capita GDP above $89K, even as growth slowed to 1.25% in 1H25 (vs. 2.8% in 2024) and July jobs came in weak at +79K. By contrast,

Moody’s downgraded the U.S. in May, citing rising debt and policy uncertainty.

Powell Signals Likely Rate Cuts at Jackson Hole

At the Jackson Hole economic forum on August 22, Federal Reserve Chair

Jerome Powell highlighted risks from both a slowing labor market and persistent inflation3,

giving markets a clear signal that rate cuts could be on the table at the September 17 FOMC meeting. Major brokerages including

Barclays, BNP Paribas, and Deutsche Bank now expect a 25-basis-point reduction, 4

which would mark the first cut since December 2024.

Bank of America, however, has cautioned against easing this year, warning of potential policy missteps without a sharper deterioration in employment.

Macroeconomic Review

GDP

The second estimate for Q2 showed U.S. GDP growing 3.3% year-over-year5,

revised up from the initial 3.0% reflecting stronger than expected investment and consumer spending.

This growth, especially supported by resilient household demand and lower imports, stands in sharp contrast to Q1’s 0.5% YoY contraction.

Federal Reserve Policy

Inflation

The headline PCE Index rose 2.6% YoY in July10, matching forecasts and unchanged from June’s pace.

Core PCE climbed 2.9% YoY, also in line with expectations, after a 2.8% gain in June.

Looking ahead, the

Cleveland Fed’s August nowcast projects headline PCE at 2.7% and core PCE at 3.0%11.

Manufacturing

The ISM® Manufacturing PMI came in at 48.7% in August, up from 48.0% in July12.

While still below the 50 threshold, the index signals that the overall economy remains in expansion for the 64th straight month, consistent with the rule that a PMI above 42.3% generally indicates broader economic growth.

The New Orders Index returned to expansion at 51.4%, a sharp rebound from July’s 47.1%, ending a six-month stretch of contraction.

In contrast, the Production Index slipped to 47.8% from 51.4%, indicating softer output.

The Prices Index stayed firmly in expansionary territory at 63.7%, though slightly lower than July’s 64.8%, pointing to continued cost pressures.

Meanwhile, the Backlog of Orders Index declined to 44.7% (from 46.8%) and the Employment Index edged up to 43.8% from 43.4%, still signaling contraction in manufacturing jobs.

Labor Market

Labor data came in notably weaker than expected13. Unemployment held at the forecasted 4.3% (up from

4.2% in July14), while non-farm payrolls increased by only 22k, well below the 75k consensus estimate and sharply lower than July’s revised gain of 79k.

Cross-Asset Performance Review

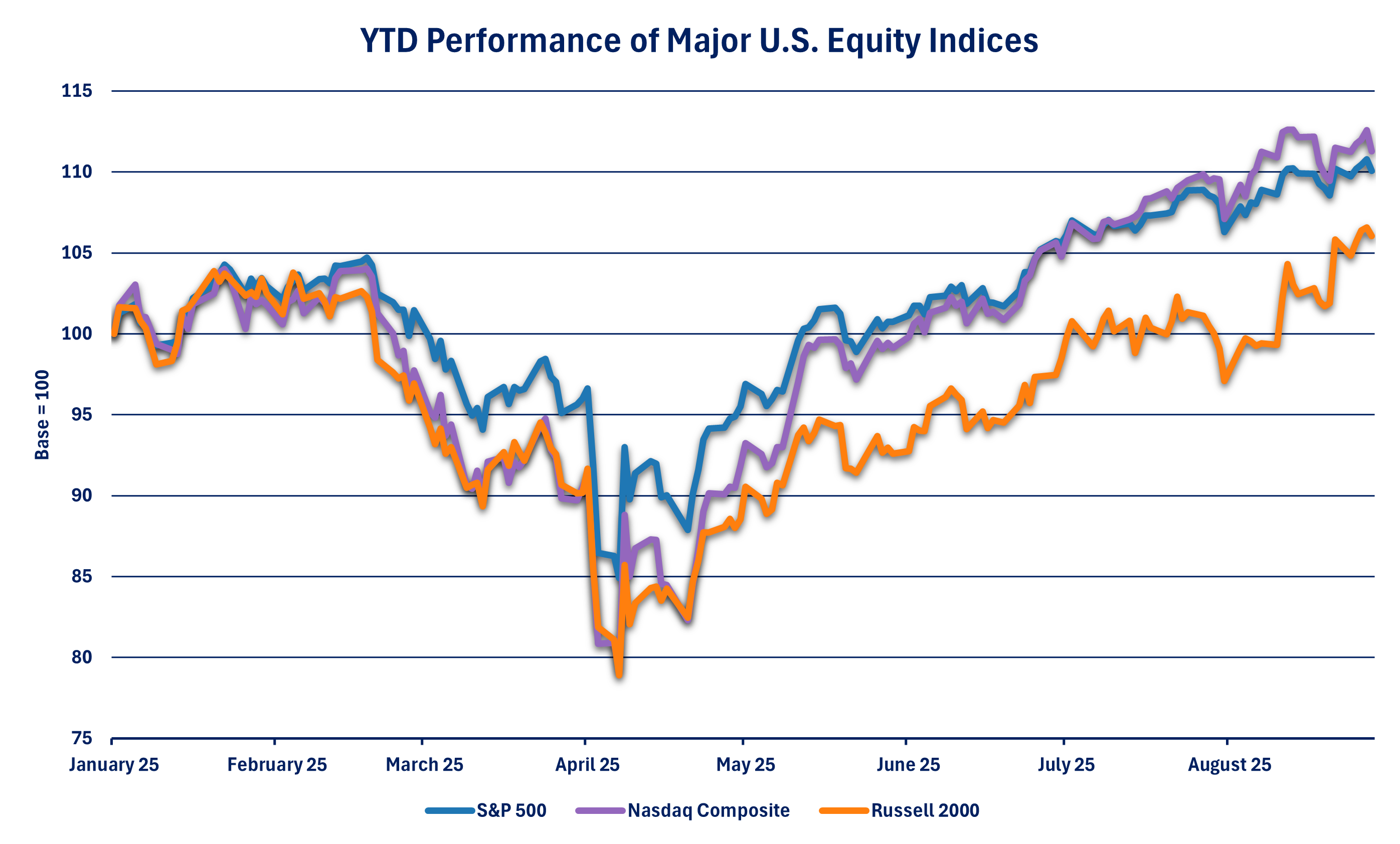

Equity Market Performance

Global equities also advanced, with the

MSCI World Index up 2.5%19.

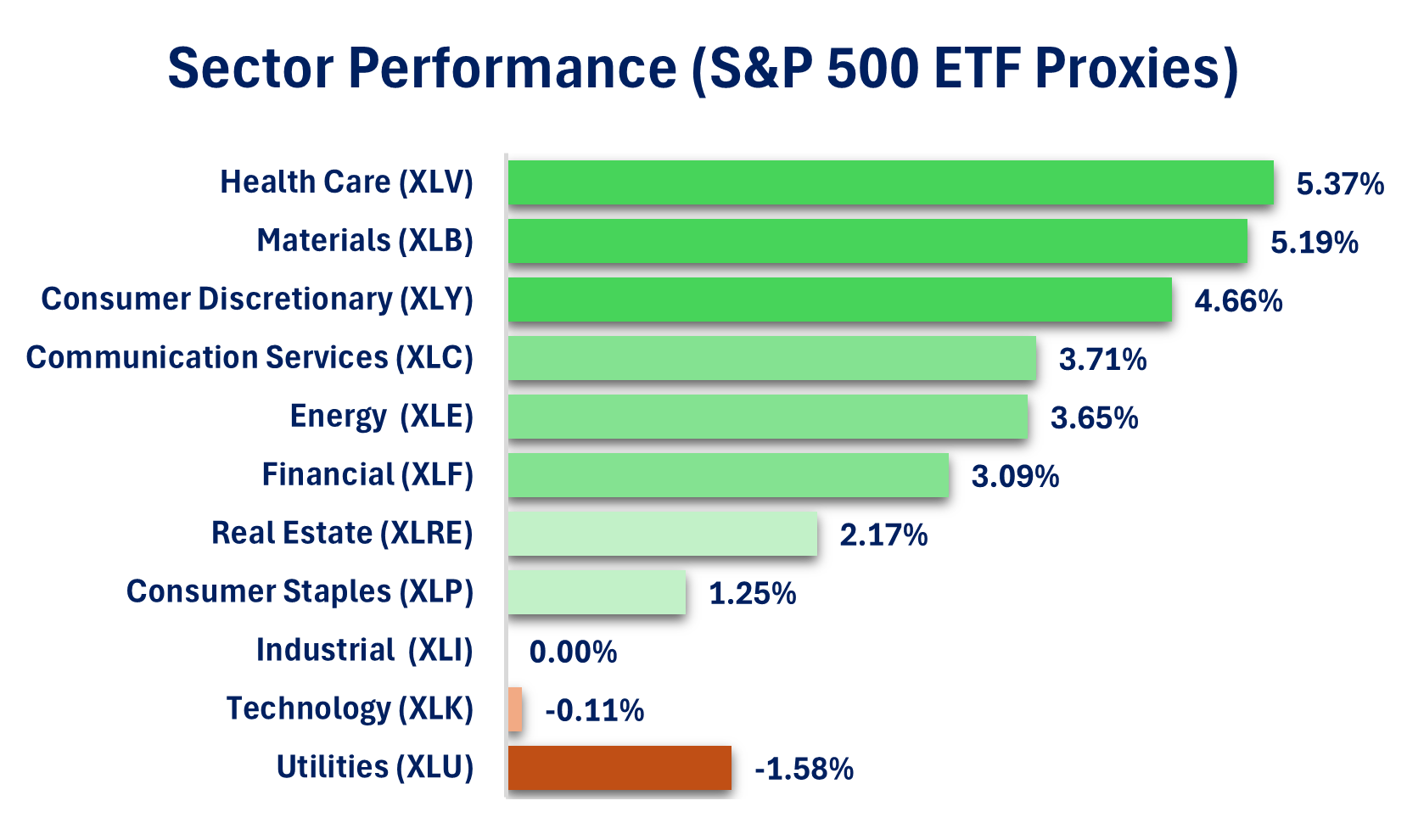

Sector Highlights

Sector performance in August was broadly positive. Materials,

tracked by the S&P 500 Materials ETF

XLB20,

Health Care (

XLV21),

and Consumer Discretionary (

XLY22) led the gains, each rising about 5%. .

Communication Services (

XLC23),

Energy (

XLE24),

and Financials (

XLF25) also advanced more than 3%.

Real Estate (

XLRE26) gained 2.17% and Consumer Staples (

XLP27) added 1.25%,

while Industrials (

XLI28) finished flat.

Technology (

XLK29) slipped 0.11%,

and Utilities (

XLU30) posted the sharpest decline of 1.58%, acting as the main drag on overall performance.

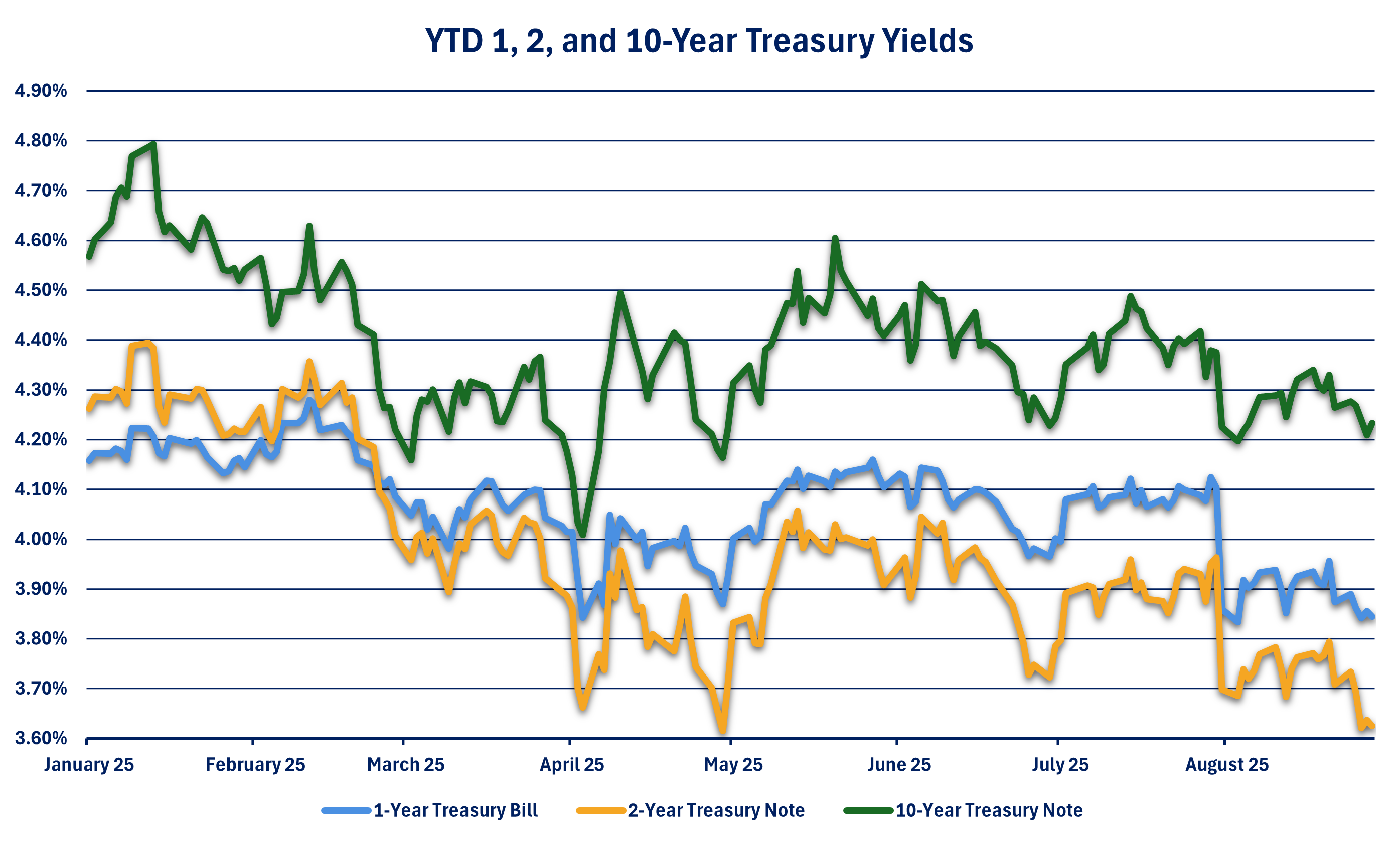

Fixed Income and Credit Markets

Treasury yields decreased across the curve, with the

one-year31,

two-year32,

and

ten-year33 down 26, 33, and 15 basis points, respectively.

The biggest drop came on August 134, after a weak jobs report accompanied by the previous downward revisions to May’s and June’s data raised expectations for Fed rate cuts.

Those expectations grew throughout the month, pushing yields lower.

Meanwhile, credit markets showed little sign of stress,

with the option-adjusted spread (OAS) on the ICE BofA US Corporate Index steady in a tight 75–82 bps range35,

underscoring stable risk sentiment through the month.

US Dollar

Sentiment

Apart from August 1, when the

VIX38 jumped to 20 on weaker-than-expected labor data and renewed tariff measures,

the index traded in a range of 14 to 18, reflecting generally calm market conditions.

Similarly, the

CNN Fear & Greed Index39 dropped to 50 (neutral) on August 1,

before rebounding into the greed zone, where it fluctuated between 55 and 66 for the remainder of the month.

ETF of the Month

Gold and Silver Miners

Gold40 and

silver41 have staged a powerful rally recently, propelled by escalating trade frictions, a weaker dollar,

and mounting expectations of rate cuts that reduce the relative appeal of interest-bearing securities such as government bonds, sustaining flows into safe-haven assets.

Gold has climbed nearly 35% year to date42, while

silver has surged about 40%, reclaiming levels last seen in 201143.

Mining equities, which typically act as operating-leveraged plays on the metals, have amplified these gains.

In August alone, the

VanEck Gold Miners ETF (GDX)44 and

VanEck Junior Gold Miners ETF (GDXJ)45 each advanced more than 20%, while their silver counterparts —

the Global X Silver Miners ETF (SIL)46 and

Amplify Junior Silver Miners ETF (SILJ)47 – rose by a similar margin.

Airline

Airline stocks surged on August 1248,

climbing more than 4% after data showed rising fares and amid expectations of reduced competition, as Spirit Airlines warned it may struggle to meet minimum liquidity requirements.

The July’s Bureau of Labor Statistics Consumer Price Index indicated carriers are regaining pricing power49,

with fares rebounding 4% after declines in June and May.

Benefiting from the improved environment, the U.S.

Global Jets ETF (JETS) – which holds nearly 50 airlines and travel-related companies –

rose almost 10% in August50.

Imperial Fund Asset Management is a SEC-registered investment adviser.

SEC registration does not imply a certain level of skill or training.

The information provided is for informational purposes only and should not be considered investment advice or a solicitation to buy or sell any securities.

All investments involve risk, including the possible loss of principal. Please review our

full disclaimer for additional information.