While there are countless technical analysis methodologies one can use, I start my work using wave-theory, a type of pattern recognition analysis.

At its simplest, wave theory describes market moves in the direction of the trend as impulse waves, with 5 internal waves labeled 1 through 5, waves 2 and 4 are corrections labeled AB&C.

The only hard rules for an impulse wave are that the 3rd wave cannot be the shortest of waves 1, 3, and 5, and that wave-4 cannot trade back into wave-1.

After an impulse wave is complete, a larger degree correction develops and that is followed by another impulse wave. I used a book with several hundred pages to learn the theory, but for the purposes of this update, those few sentences should suffice.

Yields rose during the first 3 weeks of May, with yield curve steepening putting more pressure on longer-dated maturities than shorter ones. The move was largely attributed to fears of rising debt and inflation.

While the 5-year spent the entire month trading within the same range it had established between April 7th and April 11th when the tariff-related volatility impacted all financial markets, the curve steepening pushed the 10-year to its highest yield since February 12th.

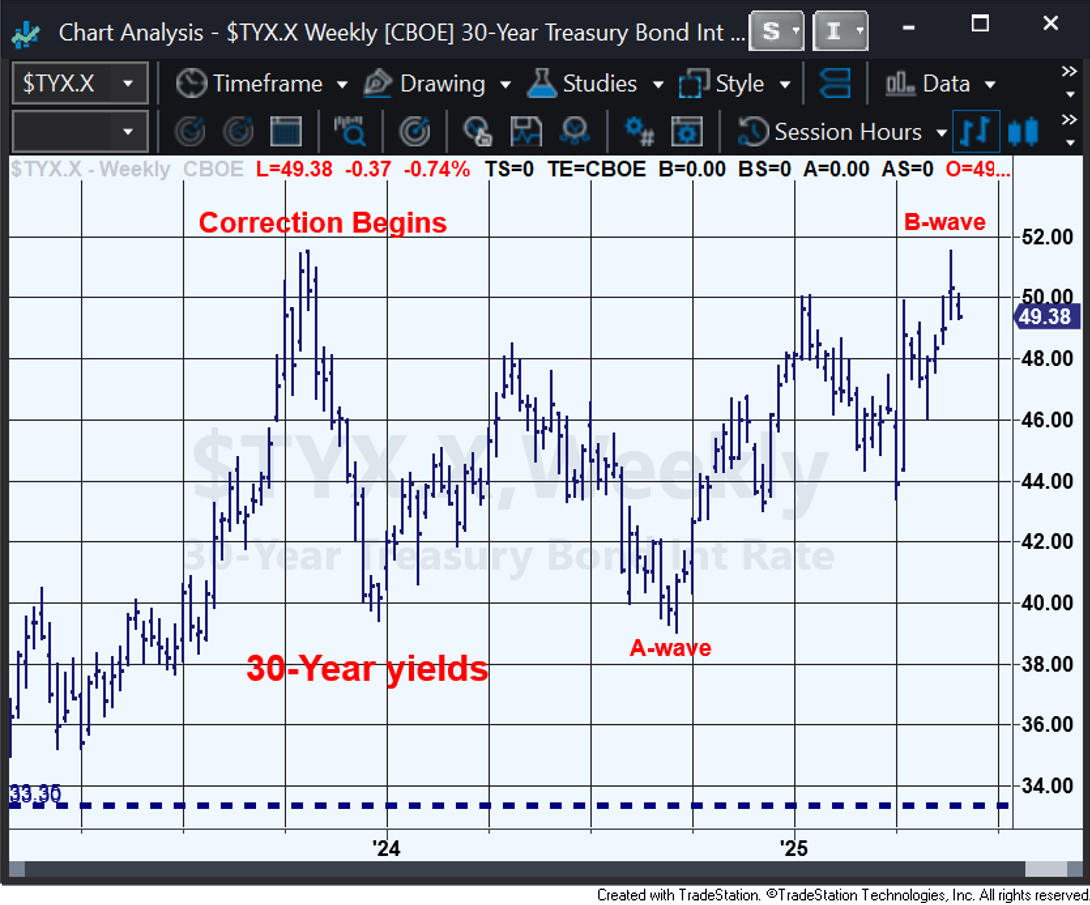

The 30-year, however, reached its highest yield since 2007 when it printed 5.157 on the 22nd.

What could prove to be most important is that in October of 2023, when yields of all the treasuries peaked after having gone from less than 1% in 2020 to around 5%, the high yield made by the 30-year was 5.152. That’s what I want to address here, but not just yet.

The wave structure of the moves from early 2020 into 2023 perfectly fit the description of impulse waves, even down to the mathematical relationships between the waves which produced terminal targets right where the moves ended. Those targets were generated while yields were still more than 100 basis points away.

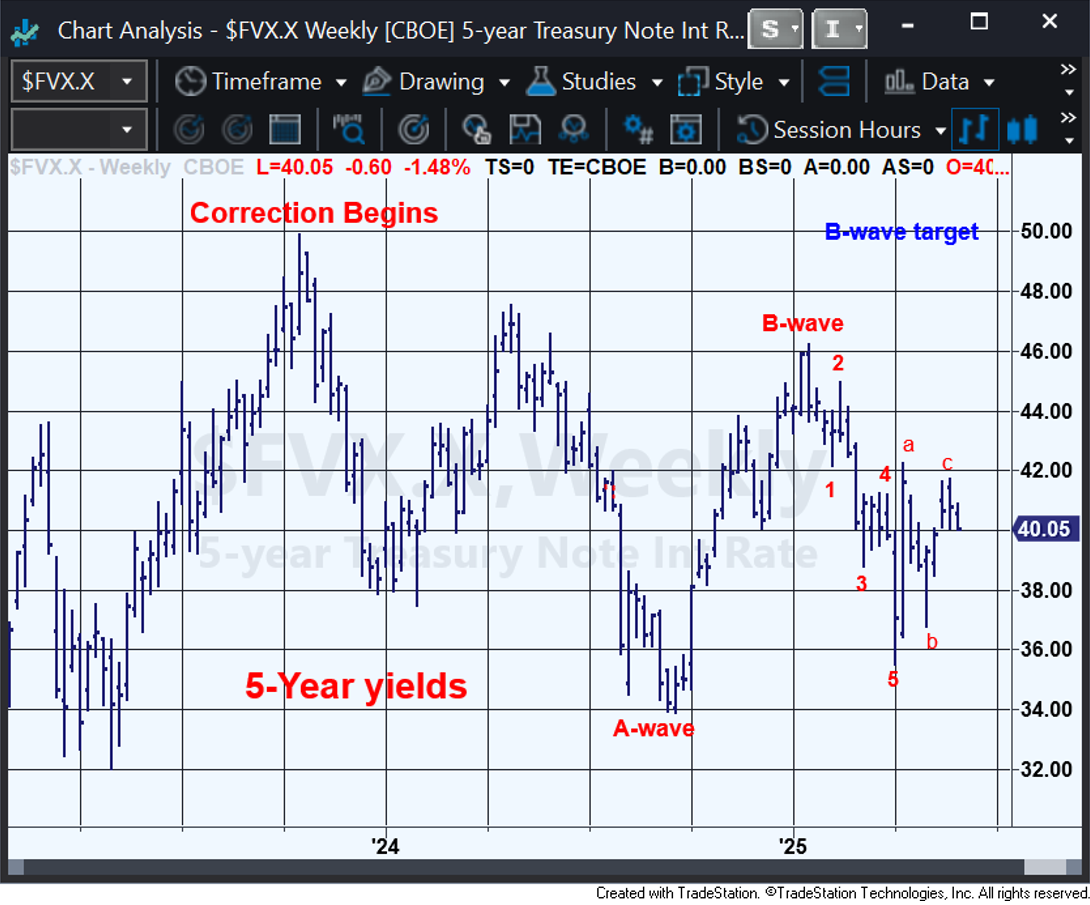

From those October 2023 yield crests, treasuries began to recover, and they rallied as much as 160 bps into September of 2024, with those rallies being clearly corrective with regards to their structure.

Wave theory teaches that all corrections which are not triangles end with 5-wave C-waves which have all the same characteristics as impulse waves. Since the rallies into September of 2024 did not fit that definition, it seemed clear based on the theory that those rallies were only the A-waves of ongoing corrections.

There are no rules for how a B-wave should look; they’re just choppy and don’t look like impulse waves. By January of this year, when yields were well over 100 basis points above the September lows, the moves which had figured to be B-waves looked as though they were.

The perfect targets for the B-waves of the types of correction that were developing—even though perfection is never something to expect—were right back where the corrections began. In this case, they were right around 5% for the 5-year and 10-year, and 5.15 for the 30-year.

In January, treasuries began to rally again, and by April 4th the rallies had reached around 100 basis points, but they ended abruptly during the tariff-related chaos.

Those rallies fit the definition of impulse waves for the 5-year and 10-year, so they looked like they could have been the C-waves of the corrections from October of 2023. However, this was not the case for the 30-year.

As yields began to rise from the April 4th low, once again the moves looked clearly corrective. However, while neither the 5-year nor the 10-year even got close to their January yield crests, the 30-year traded through its January yield crest and right on up to that 5.157 yield crest on May 22nd.

While perfection may not be what one should expect, with the 30-year having for its B-wave target 5.152, and seeing it reverse from a trade at 5.157 after having been at 3.90 in September, 4.35 on April 4th, and 4.62 on April 30th, that’s about as perfect as a target can get.

So, how does one connect the dots? For now, I believe that the only way to explain what has happened using wave theory is to conclude that the 5-year and 10-year completed their B-waves in January a little short of their targets, while the 30-year ended its B-wave on May 22nd right at its target.

The impulsive-looking rallies by the 5-year and 10-year from January would be the first of what should be 3 impulses down in yields, while the 30-year treasury would be just beginning its C-wave. If yields head back up now and the 30-year yield can’t hold 5.157, then I would conclude that the treasuries were still in their B-waves.

A last potential piece to the puzzle comes from a hybrid chart I created. Due to major yield curve steepening for the past several years, it has been clear that the B-wave targets would not work for all 3 maturities—and in fact, it was never a bad guess to think they wouldn’t work for any of them.

With that in mind, I created my own chart which plots the total yield of all three maturities, which in October of 2023 reached 15.15%. So, if my analysis is correct and the moves up in yield from September are B-waves, I now have 4 target areas to look for, and so far, one has worked to perfection.

Below are weekly charts of the 5-year, the 10-year, the 30-year, and my hybrid chart plotting the total yield of the three. I’ve labeled the charts to show how I view what has happened since October of 2023.

Included in my labeling are the B-wave targets for the 3 charts which have not yet achieved them, and while they still might, I’m heading into June with a good deal of optimism.

Last month I promised to show how well some technical levels worked during the chaotic days of early April and I still plan to do that, but in the spirit of keeping this update of reasonable length, that will have to wait.

Imperial Fund Asset Management is a SEC-registered investment adviser.

SEC registration does not imply a certain level of skill or training.

The information provided is for informational purposes only and should not be considered investment advice or a solicitation to buy or sell any securities.

All investments involve risk, including the possible loss of principal. Please review our

full disclaimer for additional information.