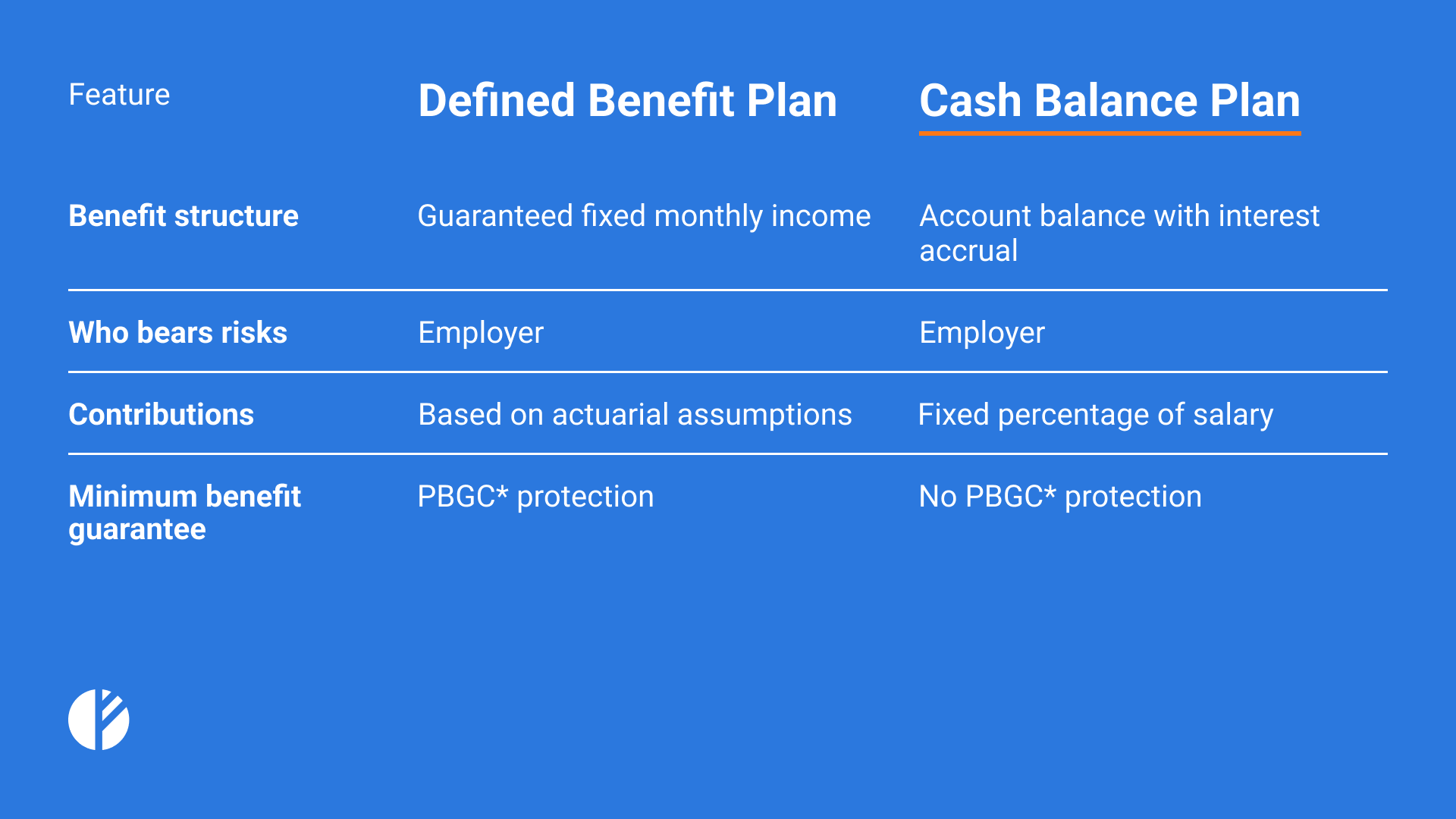

A Cash Balance Plan (CBP) combines the reliability of traditional pensions with the flexibility of Defined Contribution Plans like 401(k)s.

CBPs provide participants with an individual account that accrues a set percentage of their salary along with interest over time, allowing the balance to grow annually.

Who benefits most from CBPs?

Business owners, high-income professionals, and small to mid-sized companies typically benefit the most from CBPs.

- For business owners, this structure offers the potential for significantly higher contributions and valuable tax advantages, along with predictable and guaranteed returns.

- It appeals to businesses with stable cash flows, as the plan requires predictable annual contributions.

- CBPs are well suited for business owners nearing retirement who want to maximize tax-deferred savings, reduce taxable income, and rapidly build wealth.

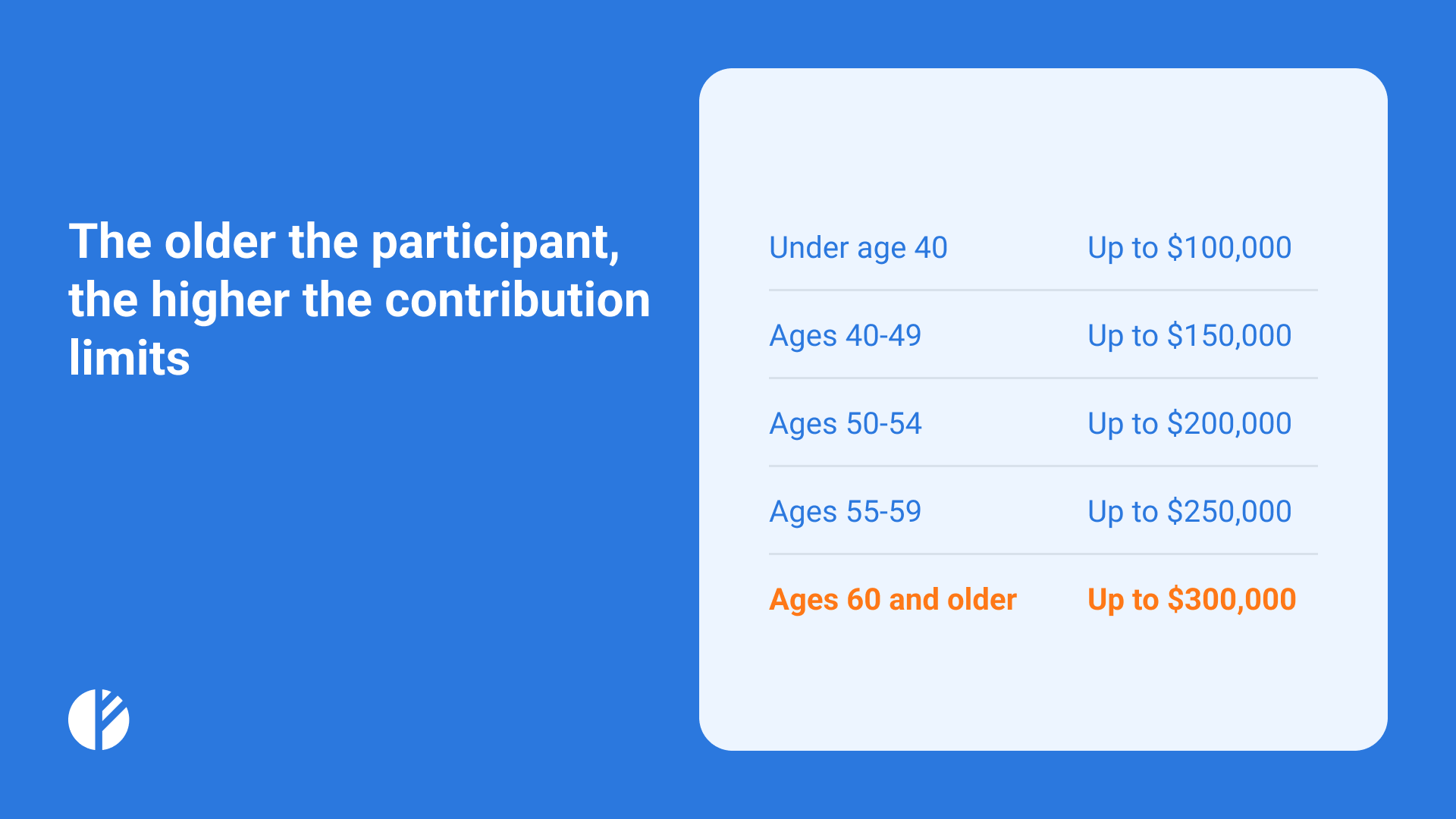

The older the participant, the higher the

contribution limits1.

What are the Risks?

Business owners should consider the risks involved:

- Financial obligations to meet guaranteed returns, regardless of market performance

- Ongoing administrative costs and regulatory compliance

- Investment risks and the responsibility for ensuring assets grow sufficiently to cover future liabilities

- Potential funding shortfalls or penalties in the event of management failure

Cash Balance Plans combine the individual account flexibility of Defined Contribution Plans with guaranteed returns and predictable contributions, providing a hybrid solution for high-income professionals and business owners.

They are perfect for individuals seeking significant tax-deferred savings and wealth growth near retirement. However, participants should be mindful of the administrative and financing risks, as CBPs come with financial obligations and require steady cash flows.

Imperial Fund Asset Management is a SEC-registered investment adviser.

SEC registration does not imply a certain level of skill or training.

The information provided is for informational purposes only and should not be considered investment advice or a solicitation to buy or sell any securities.

All investments involve risk, including the possible loss of principal. Please review our

full disclaimer for additional information.