June marked a transition toward a more balanced economic backdrop, as U.S. equities pulled back modestly, with technology and communication services lagging while industrials, financials, and small-cap value led a rotation into more cyclical, defensive corners of the market.

Oil posted its steepest monthly decline since the pandemic as the Iran conflict moved toward a fragile ceasefire, and Treasury yields fell across the belly and long end of the curve even as the front end rose. The Federal Reserve, under new Chairman Kevin Warsh, held rates steady while signaling a more hawkish policy path for the rest of 2026.

Macroeconomic Review

Inflation

The latest official inflation data available at publication covered May 2026, released in June. Headline CPI rose 0.5 percent month over month and 4.2 percent year over year, up from 3.8 percent in April and well above the Fed's 2 percent objective.

Core CPI, which excludes food and energy, rose 0.2 percent in May, down from 0.4 percent in April, with the year-over-year rate at 2.9 percent.

Energy remained the dominant driver, with the energy index up 3.9 percent in May after a 3.8 percent April rise, accounting for most of the monthly all-items gain.

The deceleration in core prices suggests the shock has stayed concentrated in energy rather than broadening into services and goods.

Whereas the Fed's favored gauge, PCE, released later in June, painted a firmer picture for May. Headline PCE rose 4.1 percent year over year, up from 3.8 percent in April and the highest since April 2023, with a 0.4 percent monthly gain.

Core PCE rose 3.4 percent year over year, the highest since October 2023, with a 0.3 percent monthly increase, both readings in line with consensus.

GDP

Real U.S. GDP grew at an annualized 2.1 percent in the first quarter of 2026, per the BEA's final estimate, an upward revision from the prior 1.6 percent estimate and a marked improvement from the 0.5 percent pace in the fourth quarter of 2025.

The revision primarily reflected stronger consumer spending and investment than previously estimated, signaling firmer underlying momentum than initially reported.

Real final sales to private domestic purchasers, a gauge the Fed watches closely, rose 1.7 percent in the first quarter, revised down from the second estimate as import and consumption revisions worked through.

Federal Reserve Policy

The Federal Reserve held its federal funds target range at 3.50 to 3.75 percent at its June 16-17 meeting, balancing persistent inflation against slowing momentum.

The meeting was also the first policy decision under Chairman Kevin Warsh, who assumed leadership in late May after Jerome Powell's departure.

The post-meeting statement was notably shorter than prior releases and dropped language signaling a bias toward future rate cuts. Warsh described the change as an effort to give investors “the facts, as best we can judge it,” rather than embed forward guidance.

The updated Summary of Economic Projections showed the median year-end 2026 rate dot rising to 3.8 percent from 3.4 percent in March, with nine of eighteen participants penciling in at least one 25 basis point hike before year-end, six projecting two.

Warsh himself did not submit a personal rate projection, a departure he attributed to a preference for reduced forward guidance.

Warsh has emphasized restoring price stability, simplifying Fed communications, and preserving the Fed's independence, consistent with the hawkish tone at the June meeting, where inflation was flagged as the primary risk despite softening labor conditions.

Manufacturing

Manufacturing activity remained in expansion during June, with the ISM Manufacturing PMI registering 53.3 percent, down 0.7 point from May's 54.0 percent, marking a sixth straight month of manufacturing expansion and, per ISM's PMI-to-GDP relationship, a 20th consecutive month of overall growth.

Underlying demand remained resilient despite signs of moderation. The New Orders Index eased to 56.0 percent from 56.8 percent, still comfortably in expansion territory, while Production fell to 52.2 percent from 54.3 percent, still indicating output growth, albeit at a slower pace.

The most notable development was a moderation in input cost pressures. The Prices Index fell 9.1 points to 73.0 percent from 82.1 percent in May, a meaningful easing in the pace of cost increases.

It remained well above the 50 percent threshold, signaling continued input price increases, though the sharp decline suggested cost pressures were beginning to moderate.

Labor Market

The June employment report, released July 2, pointed to a meaningful slowdown in hiring. Nonfarm payrolls rose by just 57,000, following a revised gain of 129,000 in May, the weakest job creation since late 2025 and well below expectations.

The unemployment rate edged down to 4.2 percent from 4.3 percent, though the decline masked underlying weakness.

Labor conditions within manufacturing remained comparatively weak. The ISM Employment Index improved to 49.7 percent from 48.6 percent but stayed below the 50 percent expansion threshold, indicating cautious hiring despite ongoing production growth.

Fourteen of 18 industries reported growth in June, down from 16 in May, with the share of manufacturing GDP in contraction ticking up modestly.

Cross-Asset Performance Review

Equity Markets

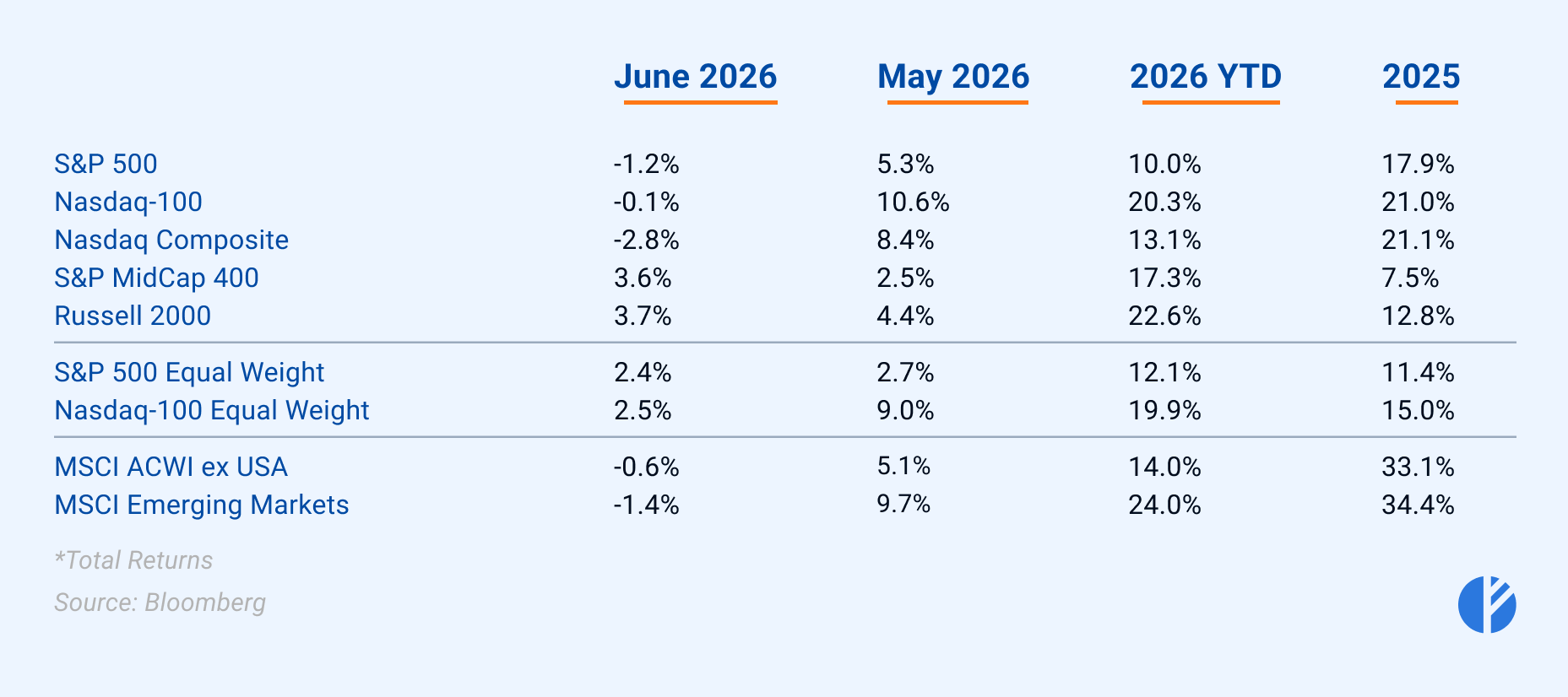

U.S. equity benchmarks were mixed to modestly lower in June, a reversal from May's broad advance. The S&P 500 declined 1.2 percent, the Nasdaq-100 was roughly flat at negative 0.1 percent, and the Nasdaq Composite fell 2.8 percent.

Mid- and small-caps outperformed large-cap technology for the first time in months, with the S&P MidCap 400 up 3.6 percent and the Russell 2000 up 3.7 percent.

International markets were mixed, with developed markets down 0.6 percent and emerging markets down 1.4 percent, both giving back a portion of May's gains.

The cap-weighted versus equal-weighted relationship flipped in June relative to May.

The S&P 500 Equal Weight index gained 2.4 percent even as the cap-weighted S&P 500 fell 1.2 percent, a 3.6 percentage point swing indicating the pullback was concentrated in a narrow set of mega-cap names rather than broad-based weakness.

The Nasdaq-100 Equal Weight Index similarly returned 2.5 percent, confirming broader market breadth beyond the largest technology names.

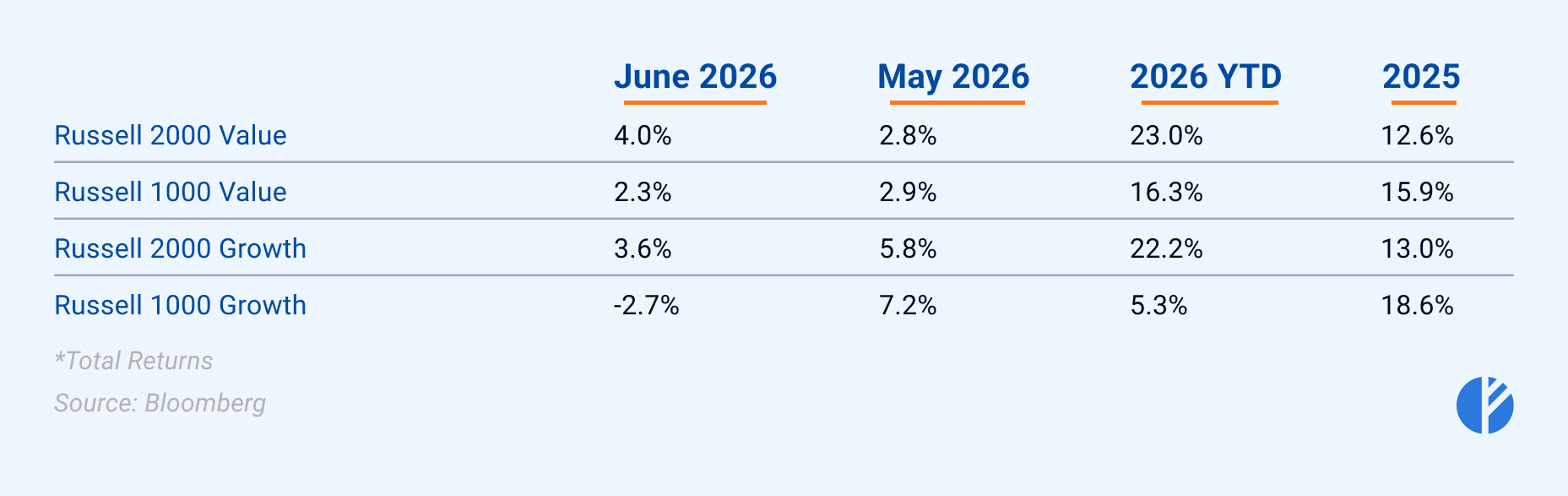

Style leadership rotated sharply. The Russell 1000 Growth Index declined 2.7 percent while the Russell 1000 Value index rose 2.3 percent, a nearly five percentage point swing from May's growth-led environment.

Small-cap value led all style and size categories, with the Russell 2000 Value index up 4.0 percent, ahead of Russell 2000 Growth's 3.6 percent gain.

Per Nasdaq's June and second-quarter review, the shift reflected investors rotating out of extended growth positions into sectors more sensitive to economic resilience and rates, though growth remained dominant for the quarter overall.

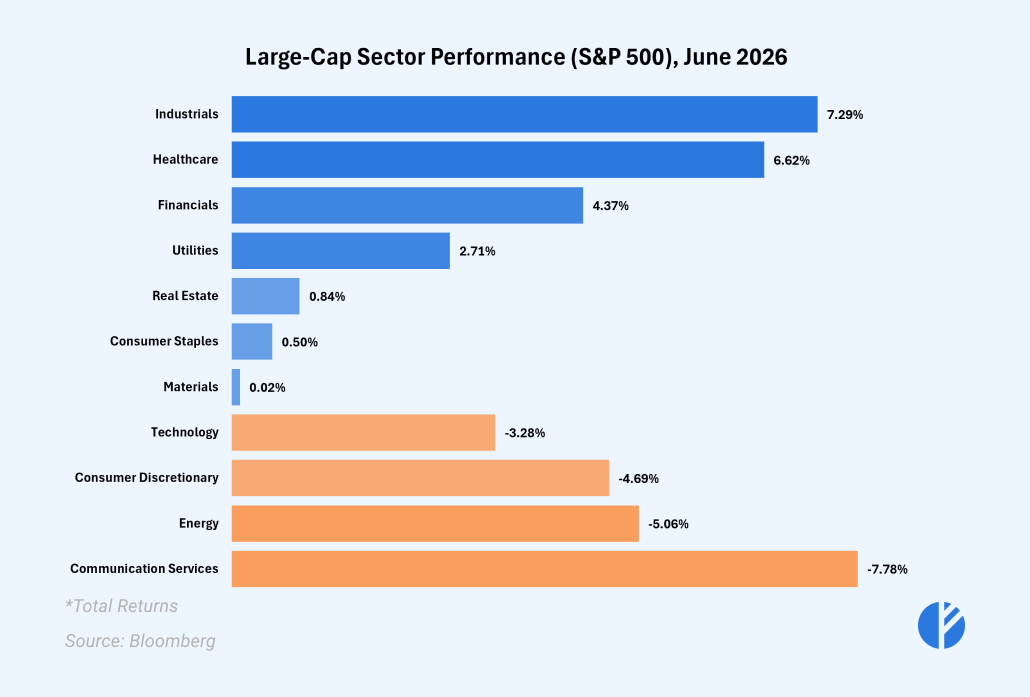

Sector performance confirmed this rotation. Industrials led all eleven S&P 500 sectors with a 7.3 percent gain, followed by health care at 6.6 percent and financials at 4.4 percent, all three having lagged in May.

Utilities added 2.7 percent, real estate 0.8 percent, consumer staples 0.5 percent, and materials were essentially flat. Technology fell 3.3 percent, giving back part of May's 16.0 percent gain, while consumer discretionary declined 4.7 percent.

Energy fell 5.1 percent for a second straight monthly decline as oil prices retreated toward pre-conflict levels. Communication services was the weakest performer, down 7.8 percent.

This broad rotation reinforces the equal-weight data above, pointing to a market that broadened out even as headline returns turned negative.

Fixed Income

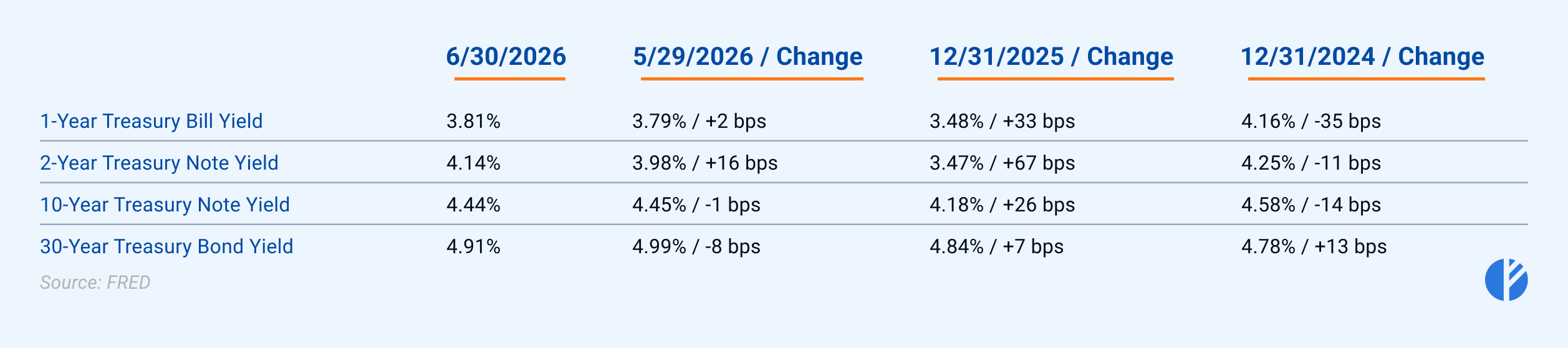

Treasury yields diverged across the curve in June, with the front end rising and the belly and long end declining, a bull-flattening move reflecting the tension between the Fed's hawkish June signaling and softening growth and labor data.

The 1-year yield rose from 3.79 to 3.81 percent, a 2 basis point increase, and the 2-year climbed 16 basis points to 4.14 percent as markets absorbed the FOMC's hawkish dot plot.

In contrast, the 10-year yield fell 1 basis point to 4.44 percent, and the 30-year declined 6 basis points to 4.91 percent, as receding oil prices and a cooling labor market tempered longer-run inflation expectations even as near-term policy uncertainty pushed short rates higher.

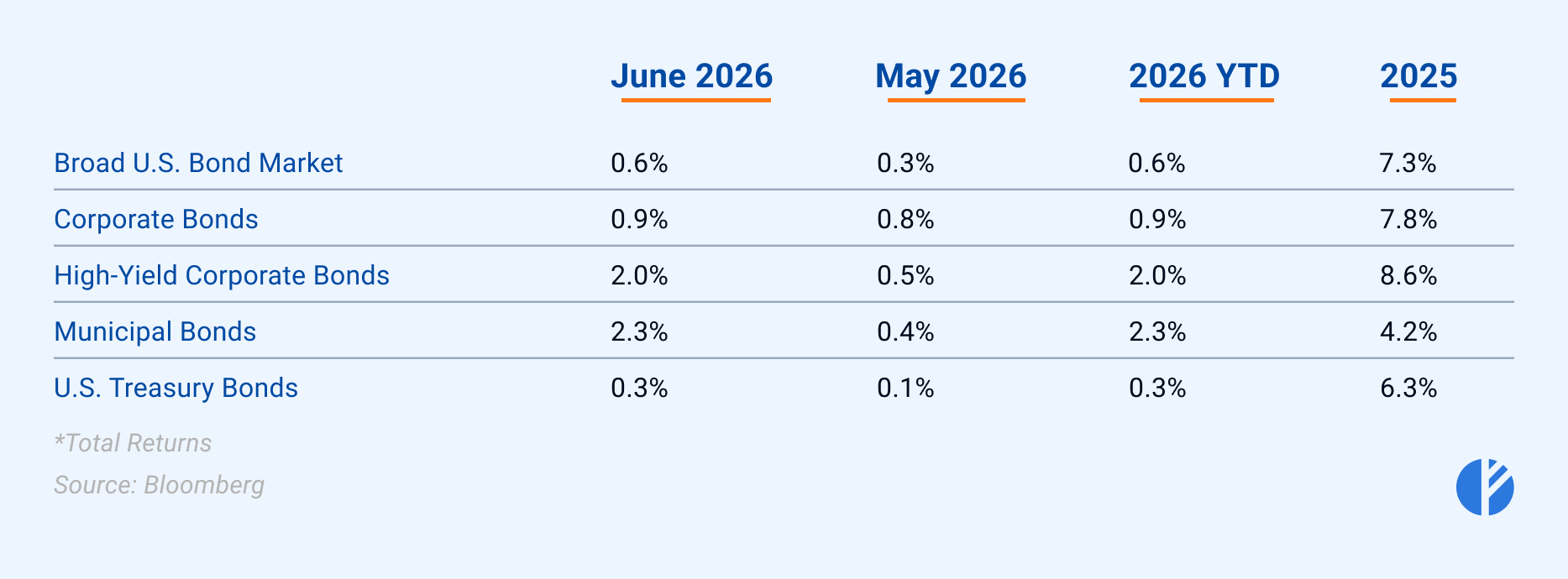

Bond index returns were positive across all major segments in June, an improvement from May's mixed picture. The broad U.S. bond market returned 0.6 percent, doubling its May gain.

Municipal bonds led with 2.3 percent, followed by high-yield corporate bonds at 2.0 percent, both accelerating sharply from May.

Corporate bonds returned 0.9 percent, while Treasuries, the laggard, returned 0.3 percent, still weakest but improved from May's 0.1 percent.

Credit spreads remained historically tight throughout June despite weaker labor data.

The investment-grade option-adjusted spread held in the high-70s to mid-80s basis point range, in the bottom decile of post-financial-crisis readings and not far from the February 2007 cycle tight.

The high-yield OAS stood at 278 basis points as of June 25, within the 270-280 basis point band that has prevailed for two months. Spreads this tight leave limited cushion to absorb shocks but signal little near-term recession risk.

Commodities

Oil

WTI crude lost approximately 20 percent in June, settling near $69.50 per barrel by month-end. Brent dropped roughly 21 percent, its largest monthly decline since March 2020, settling near $72.92.

The selloff extended May's decline, with Brent down approximately 38 percent for the quarter, its steepest quarterly drop since early 2020.

The primary driver was de-escalation of the Iran conflict. A ceasefire agreement and accompanying memorandum of understanding, reached in mid-June,

established a framework for reopening the Strait of Hormuz and initiated talks on Iran's nuclear program, reducing the geopolitical risk premium that had supported prices through the first half of the year,

even as intermittent ceasefire violations kept some market volatility.

Precious metals fell sharply in June, reversing course after a more resilient May. Gold declined approximately 11 percent for the month, closing near $4,015 per ounce,

its worst monthly decline in some time and consistent with reports describing gold's second quarter as its weakest in thirteen years.

Central bank gold demand remained a persistent offsetting factor through the quarter, but this was not enough to prevent a substantial pullback as rate-hike expectations built.

This article draws on data and insights from the U.S. Bureau of Labor Statistics (BLS), the United States Joint Economic Committee, the Institute for Supply Management (ISM), the Federal Reserve Bank of Atlanta,

Bloomberg, and FRED (Federal Reserve Economic Data), as well as leading financial publications including CNBC, MarketWatch, Reuters, Fortune, MSN, and Nasdaq.